Cost sharing reduction (CSR) payments are offered to low-income individual insurance buyers under the Patient Protection and Affordable Care Act (ACA). Such payments are provided through silver plan variants (73%, 87% and 94% actuarial values) with reduced cost-sharing requirements relative to the standard silver plans (70% actuarial value). These variants are part of the standard plan and are customer-facing. Prior to October 2017, the difference in costs to insurers between the standard silver plan (70%) and the silver plan variants (73%, 87% or 94%) were reimbursed by the federal government. After the reimbursements were defunded, insurers had to increase premiums to offset the CSR costs not being reimbursed in the silver plan variants. These adjustments are often referred to as “CSR loading.”

Since CSR loading increases premium costs on silver plans that determine subsidies, they also increase federal payments for premium tax credit (PTC) subsidies. Guidance from the US Department of Health and Human Services (HHS) on silver plan pricing has evolved over time.[1]

There are three types of CSR loading:

- Broad loading: Increase premiums for all metal level variants in the individual exchange market.

- Silver loading

- On/off exchange: Increase premiums for all silver plans.

- On-exchange: Increase premiums for only on-exchange silver plans. This has the highest impact on PTC subsidies.

Increased PTC subsidies can lead to relatively cheaper bronze and gold plans for subsidized members since subsidies are determined based on the second lowest cost silver plan in the market.

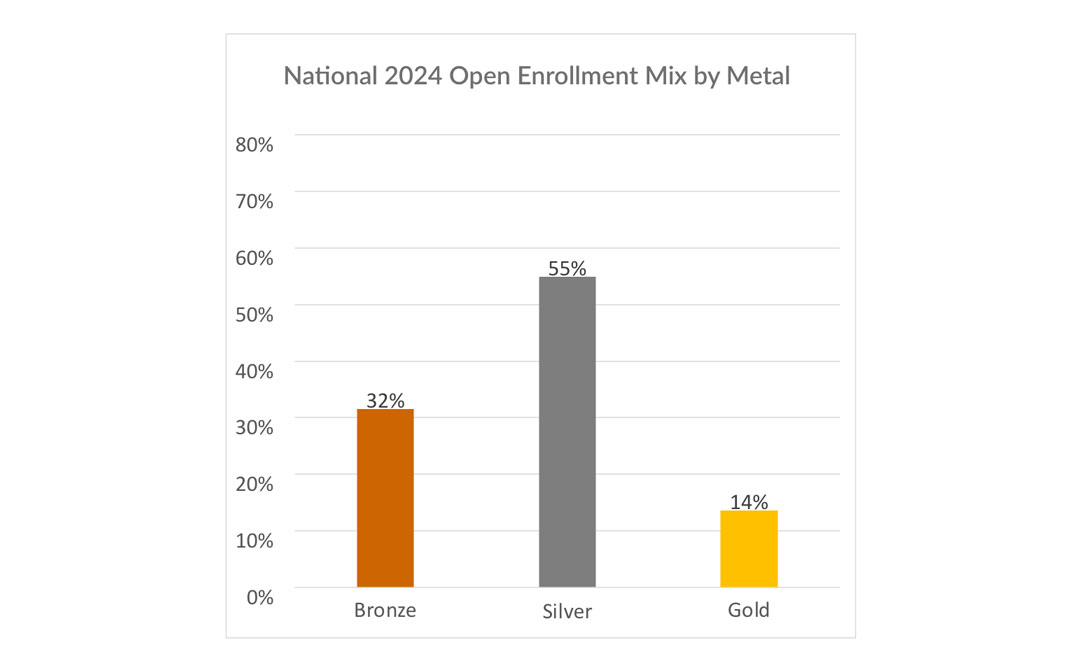

Some interesting differences are emerging between states, as they approach silver loading differently. For example, New Mexico has mandated a 44% silver CSR load, which assumes only the richest silver plan variants will be purchased and results in premiums that more closely match true plan costs. This generally results in the PTC subsidies being funded to the greatest degree by the federal government and makes gold plans cheaper than silver plans, which is not the pattern seen in other states that don’t mandate silver CSR load levels. In 2024, silver plans were typically 20% more expensive than gold plans (with some outliers), and only one in five carriers offered a bronze plan, as seen in Figure 1.