De-risking Strategies of Defined Benefit Plans: Empirical Evidence from the United States

By Steven Siegel

Retirement Section News, May 2021

Pension plan risk is among the top concerns of many organizations today as they better recognize the cost and volatility of their defined benefit (DB) plan obligations. As a result, pension plan de-risking strategies have been an area of focus for actuaries, investors, analysts and other plan stakeholders. In keeping with its goal to provide relevant research for Retirement Section members working with these plans, the SOA published a research report in November 2020 assessing de-risking strategies for U.S.-based companies. The report, “De-risking Strategies of Defined Benefit Plans: Empirical Evidence from the United States” was authored by Dr. Ruilin Tian and Jeffrey Chen from North Dakota State University as part of the SOA’s Aging and Retirement Strategic Research Program. This article provides a brief overview of the report including key takeaways.

For background purposes, de-risking has been a topic of interest for SOA research for many years. In 2014, the SOA published “Pension Risk Transfer-Evaluating the Impact and Barriers for De-Risking Strategies” authored by a team from Deloitte Consulting. In that report, the Deloitte team developed a framework that plan sponsors could use to determine their “de-risking readiness” as well as provide an extensive guide on all aspects of pension risk transfer to help retirement practitioners gain a solid understanding of the current environment. The report is currently being updated and will be published later this year.

A major focus of the 2020 report was the creation of a database of U.S. de-risking transactions from 1994–2014 using several sources including the SEC’s Electronic Data Gathering, Analysis and Retrieval System (EDGAR) and firm-level financial data from Compustat. Using this data, the report evaluates a wide range of de-risking strategies including shifts (from DB plans to defined contribution (DC) plans), freezes, terminations, buy-outs, buy-ins, longevity hedges and liability driven investment (LDI). The report includes a detailed description and environmental history on each of the strategies to help readers understand how they differ and the magnitude of their risk impact.

A primary challenge of this research effort was the identification of the individual de-risking transactions recorded in the various data sources. Data techniques including web crawling, text mining, machine learning and manual judgement were employed to first identify the transactions and in turn, build the database. With this data, the resulting report represents what is thought to be the first such study to explore U.S. de-risking activities with a relatively complete range of empirical data. In addition, another important outcome of the work is that the suite of techniques used for identifying transactions in the report provides a foundation for their application in other research projects with similar data challenges.

Once the database was complete, the authors then conducted extensive univariate and regression analysis incorporating a variety of measures prior to, during and after de-risking occurred.

High level observations from the statistical analysis include:

- Firms with low profitability, poor pension funding status, high pension asset beta (beta of a company without the impact of debt), or high earnings/stock volatility are more likely to de-risk DB pension plans.

- Economic downturns and lower interest rates are driving factors of pension de-risking.

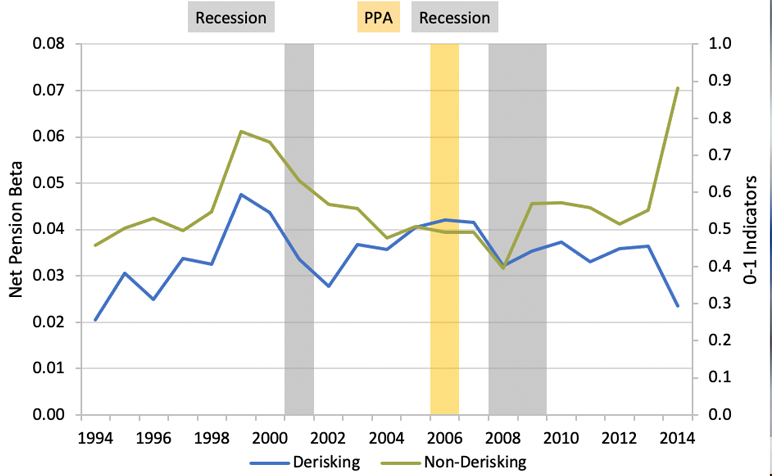

- De-risking increases long-term shareholder value and reduces net pension beta (the difference between pension asset beta and pension liability beta). Figure 1 shows a comparison of net pension beta between de-risking firms and those that have not de-risked with reference to periods of recession and the introduction of the Pension Protection Act (PPA) in 2006.

Figure 1

Net Pension Beta

At the time of the study, data was available for analysis from the time period of 1994–2014. Future follow-up efforts may be focused on expanding this time period with more current data and extending the analysis with data from other countries. Other potential future projects may include further exploration of related causal relationships such as that between executive compensation and de-risking, and more detailed investigation of individual de-risking strategies.

Special thanks to the oversight group members recruited for this effort for their expert guidance in completion of the report: Caspar Young (chair), David R. Cantor, Michael S. Clark, David DiMartino, Frederic Kibrite, Steven H. Klubock, Jesse Millner, Xingyu Pan, Max J. Rudolph, and Lisa Schilling. Their thoughtful feedback throughout the course of the work was invaluable.

Finally, I’d encourage you to read the full report and contact me with any thoughts you might have for future efforts in this area. And be sure to look for the update to the “Pension Risk Transfer-Evaluating the Impact and Barriers for De-Risking Strategies” report mentioned earlier and coming out later this year.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries, the editors, or the respective authors’ employers.

Steven Siegel, ASA, MAAA, is a research actuary with the Society of Actuaries. He can be contacted at ssiegel@soa.org.