How Do You Value Priceless?

By Chris Droussiotis

Risks & Rewards, February 2023

I recently spoke to a scientist and inventor to help him commercialize his product. After he demonstrated his brilliant new product, I asked a basic question: What do you think your invention is worth? “Priceless,” he said. I realized that I knew the answer before I asked it. It is like asking what your newborn is worth.

Introduction

Investment opportunities are frequently analyzed, identifying the risks, and valuing the business through building spreadsheets. However, valuing a company or an investor’s equity is highly subjective. There is a lot of interpretation of the data used in valuation methods. Valuation is both art and science. There is judgment in data selection. Buyers and sellers have different perspectives, resulting in differing valuation assessments. Even with all the analysis, the value of anything is what someone is willing to pay.

That not all valuations can be calculated accurately on spreadsheets is evident from financial history. How can one explain the stratospheric growth in stock prices for many technology companies that had negative income and cash flows for many years in their early stage of development (e.g., Amazon or Facebook)? U.S. FinTech company Venmo raised $1.5 million in seed money, and in less than three years was bought by PayPal for $800 million.

One important lesson is that a valuation not supported by a story is insensitive. People remember stories better than spreadsheets. Successful investors are often willing to expand beyond the traditional valuation methods and incorporate new metrics. The resulting model combines old valuation methodologies and storytelling.

How are new ideas valued? How are values determined for intellectual property, a brand name, a franchise, a trademark, or a new start-up? Valuing intellectual property is critical given the high growth of new technological platforms such as FinTech, CleanTech, HealthTech and EduTech. It is no coincidence that the largest companies by market cap are technology companies such as Apple, Amazon, Google & Microsoft. All three started with convincing storytelling. A good story is simple, credible, and persuasive.

The remainder of this article describes methodologies used to value companies at various stages of development. As shown later, they can also be used to value a product or intellectual property.

Business Valuation Overview

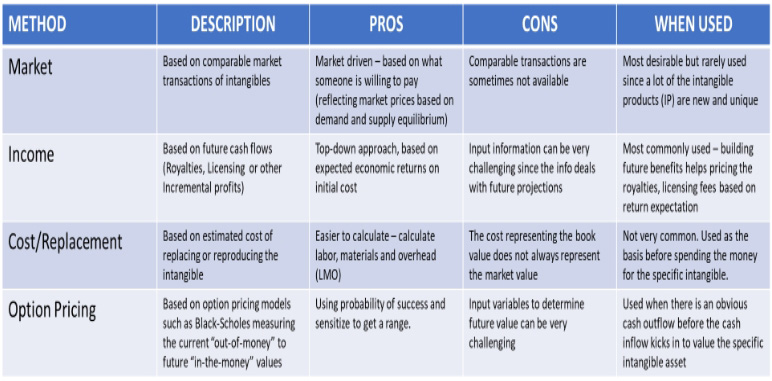

There are many methods for valuing companies based on their life cycle stage including “idea” companies that own intellectual property, young companies that sell to one or two customers, mature growth companies, mature companies, declining companies, and distressed companies. All can be valued using one of the traditional methodologies described in the following table.

Methods of Valuations Explained

Market methods include using the stock price as measurement of value for a public traded company; using comparable trading values of other similar companies in the same industry; and using other comparable companies that have already been purchased by strategic and/or private equity investors, called acquisition comparable.

Income methods include the discounted cash flow method (DCF) that derives company value as the present value of its future cash flows; and the leveraged buyout method (LBO) that derives company value based on what a private equity investor is willing to invest to meet their return targets.

Cost or cost-to-duplicate and replacement methods include methods that are derived starting from the actual cost of development to companies that are going through liquidation or bankruptcy where the value could be lower than the original investment.

Option pricing methods include methods that use closed formulas, such as the Black-Scholes option pricing model and other probability of success models to calculate company value. These methods are primarily used for “idea” companies or start-ups that do not generate income or cash flow, and distressed companies that have negative income and cash flows.

Each method has its pros and cons. It is important to choose one that is in line with the company’s life cycle stage. The following describes which methodologies are appropriate for each stage of development.

A. Valuing Well-Established Companies

These are companies that have at least five years of operating history. Having five years of operating performance is a good indication of future performance unless there has been a clear shift in the business. Historical revenue growth and operating and capital costs as percentage of revenues can be used as the basic drivers for building projections.

A.1 Income Methods

Discounted Cash Flow Method (DCF)

This method values the company based on four variables: 1) future stream of cash flows derived by revenue growth and cost assumptions; 2) exit year—typically five years; 3) the value of the company at the exit year (terminal value); and 4) the discount rate (DR), which represents the expected return based on the risk of success. The enterprise value (EV) using a DCF is:

EV = Equity Value + Current Debt - Current Cash.

Equity Value is determined using the following formula:

where CF is the future equity cash flows, t are the years, n is the exit year, ![]() is the discount rate, TV is the value of Equity at the exit year.

is the discount rate, TV is the value of Equity at the exit year.

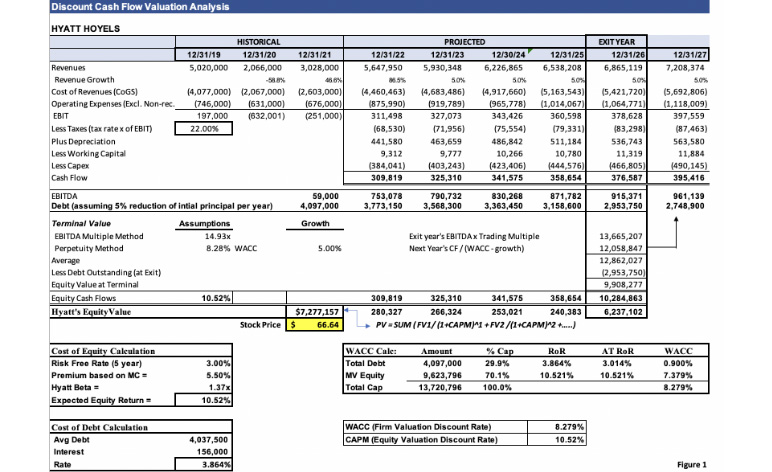

The following example (Figure 1) shows a summary of the DCF value of Hyatt Hotels, a publicly traded company with stock price at $88.13 as of November 11, 2022:

Figure 1

Summary of DCF Value of Hyatt Hotels

The DCF valuation projects the company’s top line revenue and bottom-line profit to determine the equity cash flow input variable. The discount rate is derived using the Capital Asset Pricing Model (CAPM). Figure 1 shows the equity cash flows generated based on revenue growth of 5.0 percent annually starting next year and costs expressed as a percentage of revenue. The terminal value is calculated using the average of two methods:

- The industry earnings before interest, taxes, depreciation, and amortization (EBITDA) multiple—in this case the hotel sector trades at approximately 14.9x EBITDA; and

- the perpetuity method, which calculates the terminal value as next year’s cash flow divided by the difference between the weighted average cost of capital (WACC) of Hyatt calculated at 8.3 percent and a 5.0 percent perpetual growth rate where:

Based on the DCF model, Hyatt’s equity is valued at $66.64 per share as compared to the existing trading value of $88.13 suggesting that this was not a good time to buy the stock.

Leveraged Buyout Method

The Leveraged Buyout Method (LBO) is a method that uses the DCF method above to first calculate the equity cash flows but further adjusts for the capital structure via financial engineering to reduce the equity need for a hypothetical purchase of the valued company—basically replacing the cost of equity with the lower cost of debt until the returns meet certain thresholds (i.e., 25 percent IRR).

A.2 Market Methods

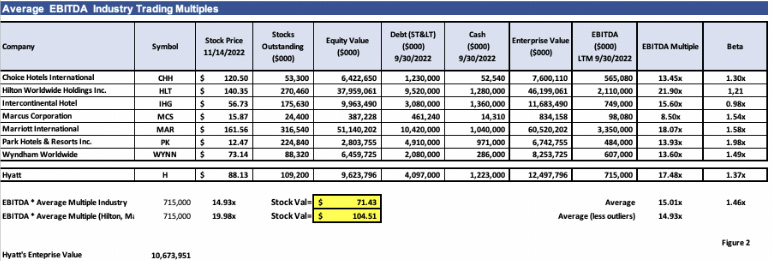

Market valuation approaches for well established companies include comparative analysis, which determines a company’s value using values of publicly traded companies in the same industry or business. For each publicly traded comparable company, the current enterprise value (EV) is calculated as follows:

EV = ( SP x SO ) + D - C

Where SP is the stock price, SO is the stock outstanding representing the number of shares the company issued since going public, D is the value of the company’s debt, and C is the amount of cash.

The example shown on Figure 2 below shows that Hyatt’s hotel peer companies have enterprise value that is on average 14.93 times their EBITDA. The value of Hyatt equity using the EBITDA trading comparable method is estimated at $71.43, as compared to the stock price at that time of $88.13. If you just use direct competitors and large rivals of Hyatt such as Marriott and Hilton that average 19.98x EBITDA multiple, Hyatt equity is valued at $104.51.

Figure 2

Hyatt’s Hotel Peer Companies Enterprise Value

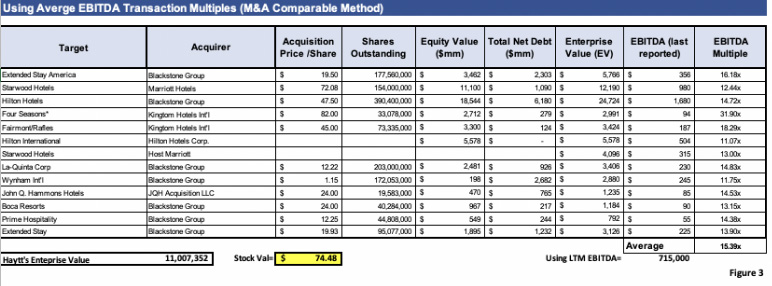

Another market-based valuation method using comparable analysis compares the company being valued to similar companies that have been acquired recently based on the ratio of the enterprise value of each acquired company to their reported EBITDA at the time of the transaction. This EBITDA multiple is used to calculate the price of the company being valued. Using Hyatt as an example, Figure 3 shows that hotel companies acquired in the last few years were purchased at 15.39 times their reported EBITDA. The value of Hyatt stock using this method is $74.48 as compared to the stock price of $88.13.

Figure 3

EBITDA of Hotel Companies Acquired Recently

B. Valuing New Ventures and Intellectual Property

For businesses with little or no reported revenue, positive cash flow or profits and an uncertain financial future are highly challenging to value. Mature public companies with steady revenues and earnings can be valued using methods that rely on EBITDA multiples. However, a new venture is usually not publicly traded and may be years away from revenues and EBITDA, making such methods inapplicable. A few methods used for determining the value of these promising ventures, of which intellectual property is a key component, are described below.

B.1 Using Cost, Cost-to-Duplicate or Replacement Method

The new venture investor first needs to calculate how much it would cost to build a similar company from scratch to compare with the one being analyzed. Savvy investors will be willing to pay more than it would cost to duplicate. This approach is easy if the focus is on tangible assets. To duplicate a software business, for example, it might be calculating the total cost of designing, programming, and the time to implement the software in the market. For a start-up in the CleanTech or FinTtech space, the costs could be for research and development, patent protection, prototype development, etc. This approach (cost-to-duplicate) should be the starting point for valuing start-ups since it is objective.

The big problem with this approach is that it ignores the company's future potential revenues and profits. It also fails to capture intangible assets, like intellectual property and brand value. A cash flow analysis is needed to calculate the immediate cash flow required for the next 18 months or so, and then convincing the investor that the product can be commercialized and scaled to market demand.

B.2 Using Market Methods

Venture capital investors prefer the market approach, as it gives them a fairly good indication of what the market is willing to pay for a company. The market multiples approach values the company against similar companies in the industry that have either been recent acquisitions or are currently traded publicly.

For example, suppose FinTech application software firms are selling for three times sales revenue. Knowing that fact, the three times sales revenue multiple can be used as the starting point for valuing a similar FinTech venture, with the multiple adjusted to account for different characteristics. FinTech software companies at an earlier stage of development than other comparable businesses would likely be valued at a lower multiple to reflect the additional risk being borne by investors.

To value a firm that has no revenue, extensive forecasts must be run to determine what the sales or earnings of the business will be once its product or service is commercialized. One way of determining such revenue is to answer the following four questions:

- What is the market size for the product?

- What are the competitive advantages of this company’s product versus those generating revenues?

- How much will it cost to implement and commercialize including customer acquisition costs?

- How long will it take before competition intensifies?

Investors willing to provide capital do so when they believe in the story. While many established corporations are valued based on earnings, start-ups are valued based on future revenue multiples.

B.3 Using Income Methods

Most start-up value is based on future potential. DCF analysis is thus an important valuation approach. DCF involves forecasting how much cash flow the company will produce in the future and then, using an expected rate of investment return, calculating how much that cash flow is worth. A higher discount rate is typically applied to start-ups, as there is a high risk that the company will inevitably fail to generate sustainable cash flows.

The limitations of DCF for start-ups lies in the ability to forecast future market conditions and make accurate assumptions about long-term growth rates. Projecting sales and earnings beyond a few years often becomes a guessing game. Moreover, DCF valuations are highly sensitive to the discount rate used. Therefore, DCF valuations of start-ups should be used with caution.

Valuation by Stage

The development stage valuation approach is often used by angel investors and venture capital firms to quickly come up with a rough range of company value. Such "rule of thumb" values are typically set by investors, depending on the venture's stage of commercial development. The further the company has progressed along the development pathway, the lower the company's risk and the higher its value. A valuation-by-stage model might look something like this:

|

Estimated Company Value |

Stage of Development |

|

$250,000 - $500,000 |

Has an exciting business idea or business plan |

|

$500,000 - $1 million |

Has a strong management team in place to execute on the plan |

|

$1 million – $2 million |

Has a final product or technology prototype |

|

$2 million – $5 million |

Has strategic alliances or partners, or signs of a customer base |

|

$5 million and up |

Has clear signs of revenue growth and obvious pathway to profitability |

The value ranges will vary depending on the company and investor. Start-ups that have nothing more than a business plan will likely get the lowest valuations from all investors. As the company succeeds in meeting development milestones, investors begin assigning a higher value.

Many private equity firms utilize an approach whereby they provide additional funding when the firm reaches a given milestone. For example, the initial round of financing may be targeted toward providing wages for employees to develop a product. Once the product is proved to be successful, a subsequent round of funding is provided to mass produce and market the invention.

B.4 Using Option Pricing Methods

Intangible assets defined as non-physical assets such as franchises, trademarks, intellectual property, patents, copyrights, goodwill, equities, mineral rights, securities, and contracts that grant rights and privileges and have value for the owner.

Valuing intellectual properties (IP) is highly challenging and requires answering the same four questions listed previously for firms with little or no revenue.

Valuing franchises and trademarks

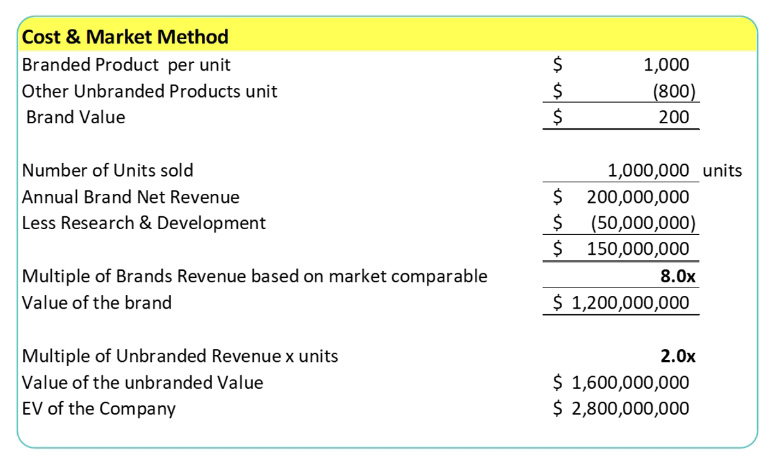

These assets do not generate immediate revenues and/or income. Since every valuation methodology depends on a projection of ongoing revenues and income to calculate value, a preliminary process is needed to establish them. Franchises and brand names establish revenue and income by comparing the difference between the revenue and income produced from non-branded companies to well recognized brand name companies. Figure 4 below demonstrates the methodology.

Figure 4 shows that a company that is well recognized such as McDonalds, Coca-Cola, or Cadbury adds significant value from the customer point of view. Franchise and brand names build customer loyalty, allowing the company to charge higher prices since the demand is more price inelastic. To value the brand name, the incremental income that is generated because of customer loyalty is estimated and separated from the unbranded product income. The branded income is valued at a higher multiple as illustrated in Figure 4. In this example the unbranded generic product is valued at 2.0x revenue based on trading or acquisition multiples and branded income is valued at 8.0x revenue.

Valuing Start-ups—Converting the Story to Value

Previous methods have discussed how to value a company depending on the stage of company development. Every company has a beginning as a new start-up. Before that there was a story, a belief, and an opportunity. People remember stories better than numbers on a spreadsheet. The challenge is to convert stories to numbers and values. In telling the story the founder or the inventor needs to articulate who wants the product, what is the market size, and how much will it cost to implement or convince an investor to fund.

There are non-traditional methods of valuing intellectual properties such as trademarks, patents and new products or new start-ups that have not yet generated any sales. An increasingly popular one is the option pricing method that values the premiums someone is willing to pay today for a future payoff. This method involves assuming of the probability of such payment to calculate the option premium required.

Using stochastic calculus, Black and Scholes came up with an approach to estimate the probability of future value or future payoff even if the value of a call option today is out of the money. Their famous Black-Scholes formula for calculating the upfront bet or premium for a European style call option (C) is

![]()

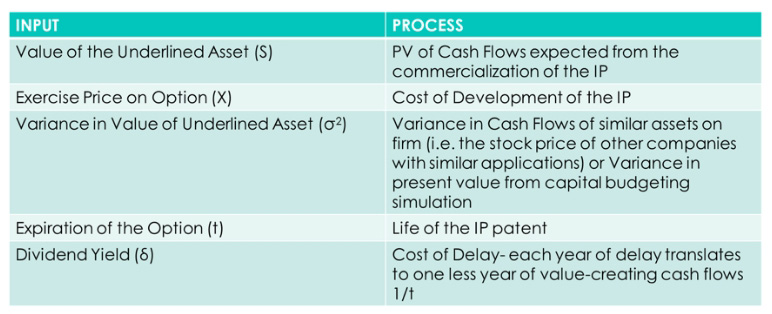

Where ![]() is the current price of the stock,

is the current price of the stock, ![]() is the exercise price at expiration, i is the risk-free rate and t is time to expiration. The formulas for calculating the probability factors d1 and d2 applied to S and the discounted value of the exercise price, respectively, are as follows:

is the exercise price at expiration, i is the risk-free rate and t is time to expiration. The formulas for calculating the probability factors d1 and d2 applied to S and the discounted value of the exercise price, respectively, are as follows:

Where σ is the standard deviation of the historical S and δ is the dividend yield.

IP and start-up companies share similar characteristics of out-of-the-money call option, and the payoff will determine the value of these asset using Black-Scholes. To use the Black-Scholes formula for valuing start-ups you need to ask the following questions to build the input information:

- Is there a real option embedded in a decision or an asset?

- Does that real option have significant economic value?

- Can that value be estimated using the option pricing model?

If the answer to all three questions is “Yes,” then the option pricing model can be used to value the start-up. The following example demonstrates how to value a start-up using this approach.

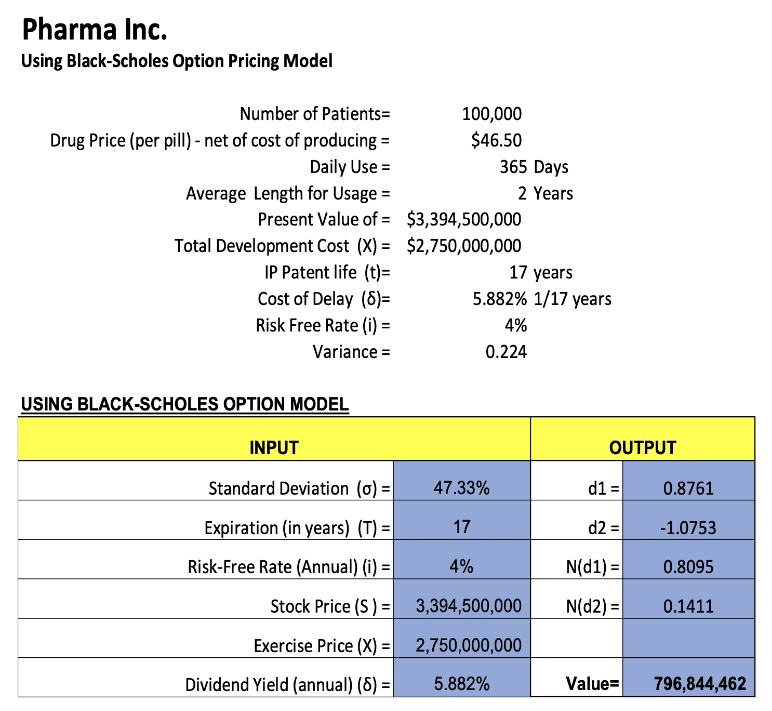

Case Study – Pharma Inc.

- Pharma Inc., a biotech firm, has a patent on a drug to treat multiple sclerosis, for the next 17 years, and it plans to produce and sell the drug by itself.

- The drug will be priced at $46.50 per patient per day taking it for an average of two years.

- After extensive market research, it was determined that 100,000 patients will be buying this drug immediately.

- The total cost of development for commercial use is estimated at $2.75 billion.

- Patent life is 17 years.

- The 17-year treasury bond rate is 3.50 percent.

- Variance in Expected Present Values = 0.224 based on industry average firm variance for bio-tech firms.

Using Black-Scholes the value of this HealthTech company is as follows (Figure 5):

Figure 5

Value of HealthTech Using Black-Scholes

Concluding Thoughts

There are many methodologies of valuing anything that has a story. The story determines how the person performing the assessment can go about approaching such assessment. In general, before we start the valuation, we ask ourselves three questions to guide us how to approach such assessment:

- How the company/project is doing versus last year or versus last few years called the Trend Analysis.

- How the company/project is doing versus their peers or the market or a specific standard called Comparative Analysis; and

- How the company/project is doing versus expectations called Expected Analysis.

Companies that are established with historical track records, compete with other companies and analysts have set expectations—basically answering all three questions—are easier to value. All methods including market, income, cost, and the option approach can be used. Start-up companies or Intellectual Properties, on the other hand, that have no history and sometimes there are not comparatives creates a larger challenge for valuing. The assessor in this case needs to incorporate other methodologies that address a simple question: What is the probability of success or what does it take to meet future return expectations? Answering the third question of expectation may involve more complex methodologies including the Black-Scholes approach of valuing “out-of-the-money” call options to measure the future possibility of a high payoff.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries, the newsletter editors, or the respective authors’ employers.

Chris Droussiotis, MBA, is senior managing director and managing partner of Kinisis Ventures and Adjunct Professor in the Enterprise Risk Management program at Columbia University. He can be reached at cdroussiotis@kinisisventures.com.