A Decade into Accelerated Underwriting: The New Normal for Advanced Risk Selection

By Lisa Seeman and Dave Goehrke

Product Matters!, August 2023

Editors' Note: This article was previously published on the Munich Re Perspectives site. It is reprinted here with permission.

Introduction

Munich Re Life US conducted its third accelerated underwriting (AUW) survey in late 2022 with the aim of capturing new and emerging trends in the U.S. individual life accelerated underwriting market. The primary goal of the survey was to compare current results to prior surveys in 2018 and 2020 to highlight key developments over the past several years. The secondary goal was to further explore the growing use of underwriting tools— particularly digital health data—in accelerated underwriting programs.

For purposes of the survey and this paper, AUW is defined as the waiving of traditional underwriting requirements (e.g., fluids, medical exams) for a subset of applicants that meet favorable risk requirements in an otherwise fully-underwritten life insurance process. This article highlights emerging accelerated underwriting trends and shares some of our high-level survey findings.

Survey Highlights

- Accelerated underwriting is now a full decade old with the earliest programs having been brought to market in 2012.

- AUW face amounts—which rapidly increased during the onset of COVID-19 in order to meet the demand for socially distant underwriting options—remained in place and even continued to grow, post-pandemic.

- Eligibility, acceleration, and offer rates also increased. However, a large proportion of AUW decisions still have some level of human involvement.

- AUW programs with higher acceleration rates share several common characteristics, with examples including multiple distribution channels and variety of underwriting tools used.

- Testing and adoption of digital health data sources, such as medical claims data and electronic health records (EHRs), is growing among carriers.

AUW Trends over Time

The 2022 AUW survey represents results from 31 companies, all with an AUW program in production as of June 2022. Earlier surveys had a similar number of participants, with slight differences in the mix of carriers represented.

Eligibility Parameters

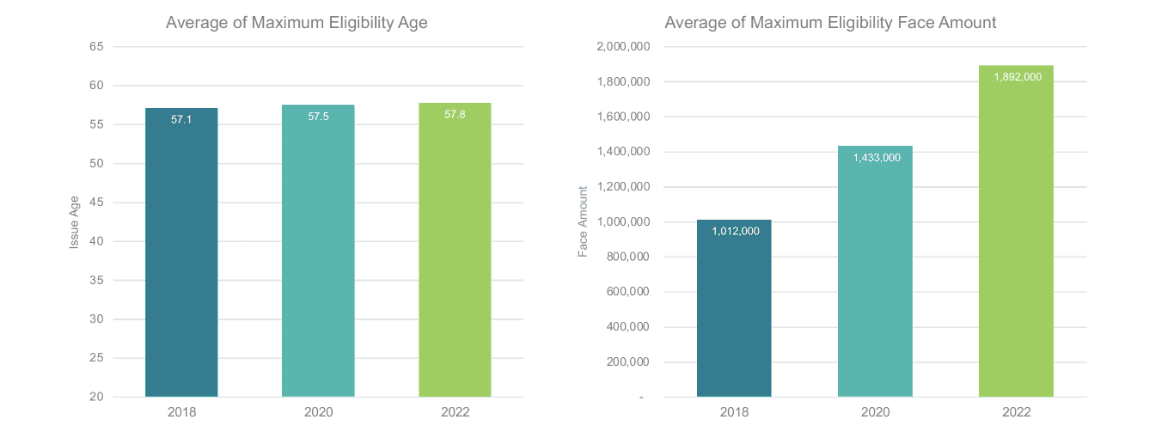

We were eager to see where the industry eligibility limits ended up in this year’s survey, given the uncertainty of the AUW face amount limits reported in 2020 (three months into the pandemic). Figure 1 depicts the change in average maximum eligibility limits over time, based on our current and past AUW surveys.

Figure 1

AUW Eligibility Trends Over Time

AUW issue age limits have remained relatively stable over time, while face amount limits continue to rise. Many of the AUW-expanded face limits we observed in the 2020 survey were initially labeled as a “temporary” quick solution for offering a socially-distant underwriting option to a broader pool of applicants. However, we later saw that not only did these programs remain above their pre-COVID limits, they also sparked a wave of secondary face amount increases later in 2020 and into 2021 from carriers that were eager to keep up with the market.

While there has been a noticeable shift in maximum face amount offerings in recent years, it is important to keep in mind that not all AUW face amounts are available to all AUW-eligible issue ages. The number of AUW programs offering a banded age and amount eligibility structure continues to grow, with now nearly half of AUW programs limiting their maximum face amount offering to younger age bands.

Product Availability

Term continues to be the most popular product offered in the AUW programs of companies surveyed in 2022, as reported by all 31 of the responding companies (100%), followed equally by universal and whole life (55% each), indexed UL (52%), and variable UL (39%).

While we saw a notable jump in AUW programs introducing permanent products between 2018 and 2020, this appears to have leveled out in 2022, as detailed in Figure 2 below.

Figure 2

Product Types Offered Through AUW Programs Over Time

Risk Class Structure

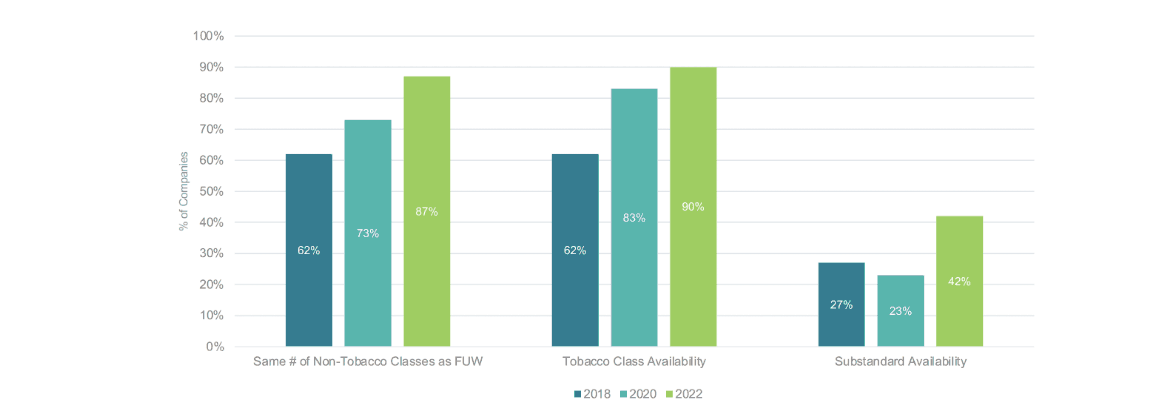

We continue to see that four non-tobacco and two tobacco classes remain the most common structure for both accelerated and traditional underwriting paths, while just under half of carriers surveyed offer substandard classes through AUW. Over time, we have seen an expansion in AUW risk class offerings as carriers become more comfortable segmenting risk with more granularity in a fluidless underwriting environment. Additional details on this evolution of risk class availability across Munich Re’s three AUW surveys are shown in Figure 3.

Figure 3

AUW Risk Class Availability Trends

AUW substandard class availability, now offered by 42% of programs, is the area with the most notable risk class expansion since our 2020 survey. This is partially attributable to the fact that several carriers restricted their substandard availability in 2020 during the initial months of the pandemic, explaining the decline in substandard offering from 2018 to 2020. However, while substandard AUW classes appear to be expanding based on reported availability, we have seen that AUW table ratings are seldom issued in practice, as more limitations are typically placed on the substandard table ratings offered through AUW compared to full underwriting (FUW).

Key Metrics

In this year’s survey, we asked participants to provide a breakdown of the total applicants across all products with AUW availability into detailed underwriting paths that would allow us to derive key performance indicators on a comparable basis across all programs. The categories included breakouts for age/amount ineligible, AUW offers, AUW declines/postpones, and those referred for additional underwriting for not meeting other AUW requirements (i.e., kickouts). The key metrics we derived from this data included the AUW Eligibility Rate, Acceleration Rate, and Offer Rate, as defined in Table 1 below.

Table 1

Eligibility, Acceleration and Offer Rate

While the industry lacks a standard definition for straight-through processing rate (STP), we know that some carriers consider STP to represent AUW decisioning without human underwriter involvement, while others offer multiple acceleration paths with varying degrees of human touch. For that reason, we expanded this year’s survey to further differentiate AUW offers and AUW declines/postpones between those that were determined with and without human underwriter review. Interestingly, we discovered that a large majority of accelerated decisions are still being made with human underwriter involvement.

Across the board, we saw a big jump in these key metrics compared to our 2020 survey. See Figure 4 for details on how these metrics trend over time, keeping in mind that the differentiation by human underwriter review was new to the 2022 survey.

Figure 4

Average Eligibility, Acceleration, and Offer Rates Over Time

Acceleration Rate Correlations

Finding opportunities to increase eligibility, acceleration, and offer rates are often top of mind for carriers when designing and enhancing their AUW programs. In order to help shed light on areas where we have observed noteworthy correlations with accelerated case throughput, below are commonly shared characteristics of AUW programs with higher acceleration rates:

- Eligibility parameters: Lower face amount limits

- Risk class structure: AUW substandard class availability

- Distribution channels : Multiple AUW sales channels

- Opt-out availability: Mandatory AUW path

- Underwriting tools: More tools/data sources in use

- Monitoring: Post-issue audit methods

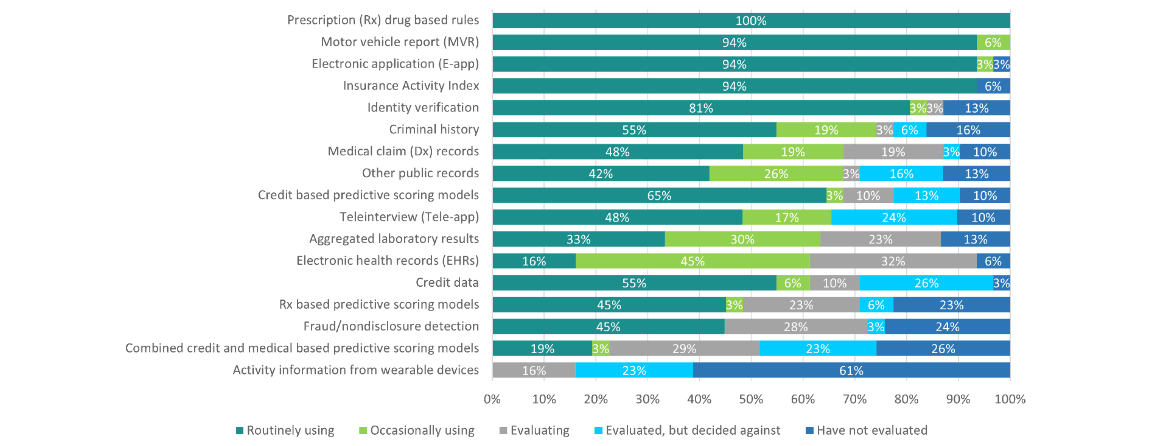

2022 Underwriting Tool Highlights

- All programs continue to use prescription (Rx) drug data and motor vehicle reports (MVR), almost always on a routine basis.

- Nearly all companies have transitioned to using e-applications, while fewer companies are leveraging tele-interviews than in prior years.

- Despite all companies using MIB, only 94% report using the Insurance Activity Index (IAI) product.

- The majority of companies are using non-medical data sources such as identity verification, credit data, credit-based scoring, criminal history, and other public records.

- Fraud/nondisclosure detection is used by just under half of AUW programs.

- Digital health data sources such as electronic health records (EHRs), medical claim records, and aggregated laboratory results are now in use by the majority of AUW programs, although not always on a routine basis.

- The data sources most likely to be used on a non-routine basis are EHRs, followed by aggregated lab results, and other public records.

- Programs continue to refrain from the use of wearable activity data in underwriting, with only a handful of companies evaluating this data source for use in AUW as of 2022.

See Figure 5 for more details on tools and information sources used by companies to triage or classify accelerated cases.

Figure 5

Underwriting Tools and Information Sources used in AUW

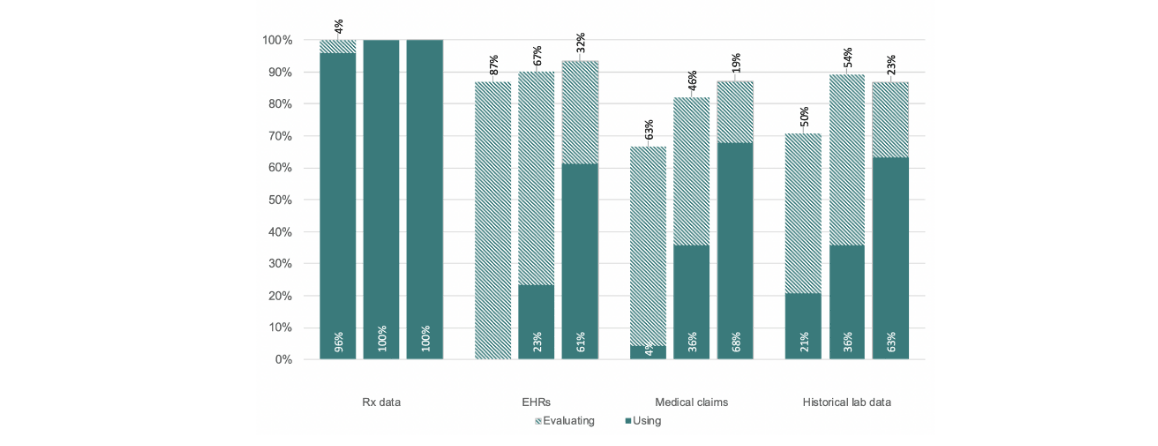

Digital Health Data Sources

Several years ago, digital health data (DHD) sources beyond Rx were not yet in wide use but were being evaluated by most companies, so it is not surprising to see that the majority of programs have now implemented them into the AUW process. Looking back, we have seen the biggest shift in the usage of medical claims data (+64%) since 2018, while EHRs have experienced the steepest adoption (+38%) since our 2020 survey. This steep upward trend can be attributed partially to the pandemic, when we saw many carriers loosen their AUW eligibility requirements to make non-invasive underwriting available to a broader segment of applicants. Carriers needed to quickly pivot their underwriting processes and integrate digital health data to gain more confidence when issuing higher coverage without traditional labs and exams. Figure 6 shows a trend of DHD evaluation and usage by percentage of participating companies across all three Munich Re AUW surveys from 2018 to 2022.

Figure 6

Digital Health Data Sources: Evaluation Versus Usage Over Time

With electronic health records (EHRs) in particular, currently the most common use case in AUW is for triage or kickout to traditional underwriting, followed by post-issue audits, and to a limited extent, in AUW rules engines with human underwriter review. However, in the future, most carriers plan to use EHRs in their AUW rules engines without underwriter involvement. While EHRs have experienced a significant increase in usage over the past several years, they are still being used on an occasional or non-routine basis more so than any other AUW tool and almost always with full review by an underwriter. This is likely a result of the hurdles of getting complete EHR data on a consistent basis.

Given the importance of reliable medical data in the absence of traditional insurance labs and exams, we think it will only be a matter of time before these emerging DHD sources saturate the market, similar to what has already occurred with prescription (Rx) history data.

Summary

As we have seen in our three surveys, AUW usage has expanded across products and risk classes, with face amounts also rising, in part due to the increased demand for fluidless underwriting brought on by the COVID pandemic. Likewise, the underwriting tools and data sources used in AUW decisioning, whether on a routine or ad hoc basis, expanded as well, led by EHRs and medical claims data. New questions in this year’s survey shed light on challenges and current limitations of AUW programs, such as the majority of accelerated decisions still extensively involving human underwriters.

In the future, we expect to see human intervention decline and digital health data sources continue to gain traction as life insurance carriers work towards optimizing their accelerated underwriting programs to issue more policies with faster turnaround times, all while remaining confident in their risk-decisioning process.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries, the editors, or the respective authors’ employers.

Lisa Seeman, FSA, MAAA, is a 2nd VP and Actuary at Munich Re. She can be reached at LSeeman@munichre.com.

Dave Goehrke, FLMI, FALU, CLU® is 2VP-Underwriting at Munich Re. He can be reached at dgoehrke@munichre.com.