Longevity Risk: What can the Past Tell us About the Future?

By Jan-Niklas Rössler and Cord-Roland Rinke

Reinsurance News, August 2023

Trends in mortality have a huge impact on the insurance industry and its products, risks and profitability. Worldwide, life expectancy has increased continuously over the past decades. However, this progress—even without considering the Covid-19 pandemic—has been subject to strong fluctuations. In recent years, an increase in volatility can be observed. Various aspects—medical science, environment, lifestyle—have influenced the trend in the past.

How can the life and health industry move forward in these uncertain conditions? In this article, we examine what has gone before and what can be learned from a closer analysis. What are the main drivers of the historical increase in life expectancy? What characterizes the dynamics of the recent past? How can mortality be projected into the future? How good are our methods of prediction and what are the risks? What risk management options are available?

The History of Life Expectancy

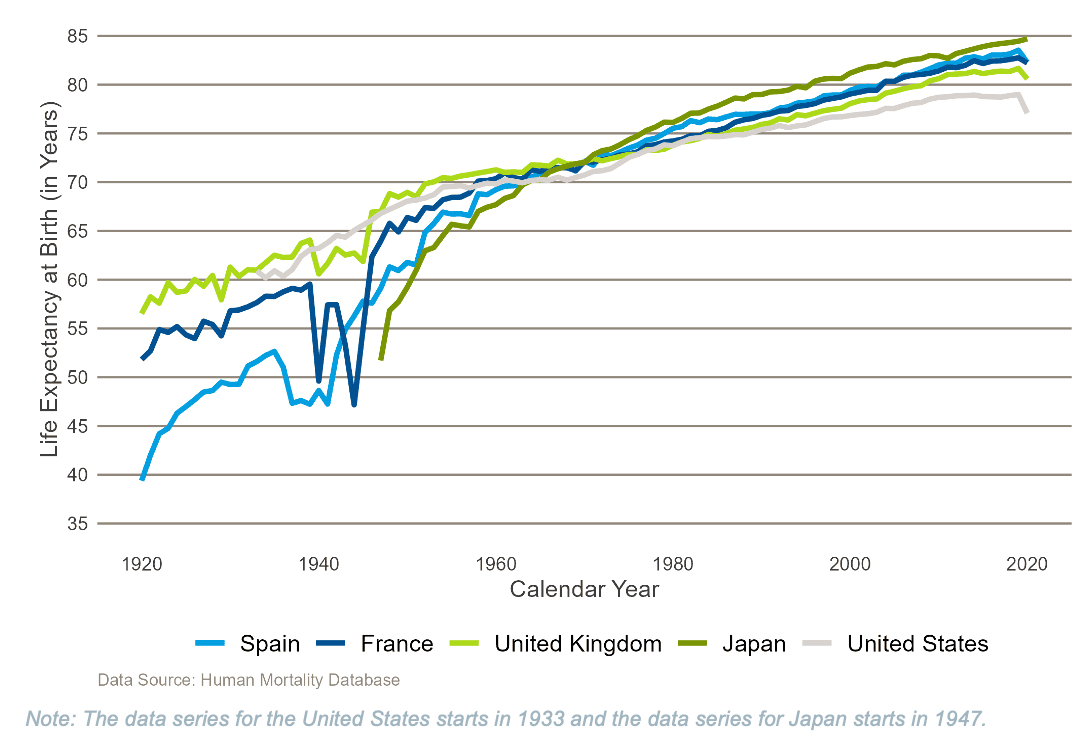

Over the last two centuries, life expectancy in industrialized countries has more than doubled. This development came with tremendous improvements in the quantity and quality of people’s lives. The trend was subject to fluctuations and regional differences, but overall remarkably stable (Figure 1). A general rule of thumb is that life expectancy has increased by about two to 2.5 years per decade during the past 50 years. While the general trend continued steadily throughout the past, the underlying drivers of mortality reductions have changed over time.

Figure 1

Life Expectancy at Birth Over Time in Selected Countries

Beginning in the late 19th century, the rise in life expectancy was mainly driven by a significant decline in infant mortality. In 1870, about a quarter of all new-borns died during their first year of life. By 1950, this figure had improved to 50 deaths per 1,000 new-borns. This reduction was achieved through improvements in environmental factors such as waste disposal, hygiene and water treatment, social advances like better housing conditions and improved air quality, as well as medical factors such as the introduction of vaccines and antibiotics. These developments led to a substantial reduction of infectious diseases and plagues, which were the primary causes of death during this period.

By the mid-20th century, infant mortality in industrialized societies had improved to such an extent that there was less scope for further reductions. However, the increase in life expectancy continued, and a decline in mortality was now observed primarily for adults. Deaths from infectious diseases decreased, but at the same time, the number of deaths from non-infectious conditions such as cardiovascular diseases and cancer increased. Since 1970, the rise in life expectancy has been driven mainly by a reduction in the mortality risk for people over the age of 65. Life spans have extended, and the risk of death has progressively shifted to older age groups. For women in the United States, for example, the risk of dying at age 85 has fallen from about 16% in 1950 to 7% in 2019. Possible reasons include people reaching older ages in better overall state of health and advances in the treatment of cardiovascular diseases and cancer, reducing the risk of premature death. In addition, environmental and lifestyle factors also played an important role. These include a healthy diet, physical activity as well as better working and living conditions, sufficient income and education.

Overall, it is difficult to attribute this remarkable demographic transition to any single factor. It was rather a complex interaction of medical, environmental, and social determinants that has driven the trend in the past. Nevertheless, current research suggests that social factors have had a far greater impact than medical advances.

Recent Trends in Mortality

Although the increase in life expectancy has been consistent over time, the journey has not been without obstacles. Wars and epidemics caused mortality shocks that temporarily interrupted the trend. The Spanish flu and the world wars are tragic examples. In the years following these events, there were some strong seasonal influenza waves, but the overall quantity and quality of shock events decreased. Recently, however, the Covid-19 pandemic caused a substantial increase in periodic mortality rates. In 2020, life expectancy declined in many countries, with only a few exceptions such as Japan and Norway. The decline was particularly sharp in the United States (-1.6 years) and Spain (-1.5 years) (Figure 1). The increase in mortality due to Covid-19 was the most significant mortality shock since World War II.

But even before Covid-19, gains in life expectancy had slowed considerably in many countries over the past decade. To describe the trend in mortality over time, we can consider mortality improvements, which measure the change in mortality from one year to the next:

For example, ix,t= 2% means that the risk of dying for a person of age decreased by 2% from year t-1 to year t.

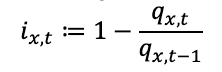

A closer look at recent trends in mortality improvements reveals some interesting dynamics. Many developed countries experienced relatively robust and regular annual mortality improvements between 1987 and 2010. In particular, the first decade of the third millennium showed remarkably high mortality improvements in many countries. However, this trend lost traction in the past decade, with average improvements between 2011 and 2019 falling well short of expectations. This was an unexpected turn, as most demographers had expected a continuing trend of strong annual mortality improvements. The slowdown was most evident in the United States, France, Australia, Germany and the United Kingdom (Figure 2).

Figure 2

Average Age-standardized Mortality Improvements Over Four Different Periods for Selected Countries

Because this phenomenon was not unique to one country, it has been the subject of debate and speculation about a global trend reversal. Possible reasons can be found in recent trends in mortality rates. Some are specific to certain countries, such as the opioid crisis in the United States. At the global level, however, the deceleration in the decline in cardiovascular disease mortality rates may be the main reason for the slowdown in improvements. In the United States, deaths from cardiovascular diseases declined by 60% between 1970 and 2010, but since 2011 the decline has stagnated. One possible explanation is the increasing prevalence of diabetes and obesity, which is currently working against the trend.

However, the trend reversal after 2010 was not entirely a global phenomenon. Switzerland, Sweden and Norway, for example, maintained a relatively strong trend between 2011 and 2019, and Japan even experienced an opposite trend dynamic with higher average improvements than in previous decades though lower than in the years from 1995 to 2003. (Figure 2).

Overall, volatility has increased in recent years, with markedly different dynamics across countries. Given current challenges such as the aftermath of the Covid-19 pandemic or the war in Ukraine, volatility is not expected to subside in the near future. The impact of Covid-19 on individual countries, for example, has been very heterogeneous. The United States recorded a deterioration of 18% in 2020, while Japan experienced improvements of +3% in the same year.

Predicting Mortality Improvements

When considering future mortality improvements, it is important to take into account the complex dynamics of the past. Accurate predictions of future life expectancy are an essential component of both pricing and valuation projections for life insurers. Demographic models commonly used to forecast mortality improvements analyze trend patterns in historical data and extrapolate them into the future. A representative of this genre of models is the age-period-cohort (APC) model. This model decomposes the historical trend into an age, period, and cohort component:

![]()

These components are all non-constant but carry different implications. The age effect (ax) includes physiological changes as individuals age and the fact that medical improvements address diseases with an age-dependent prevalence. The cohort effect (yt-x) reflects changes in mortality across different generations with varying historical experiences. The period effect (kt) represents a variation over time (i.e., calendar years) that affects all age groups and birth cohorts simultaneously.

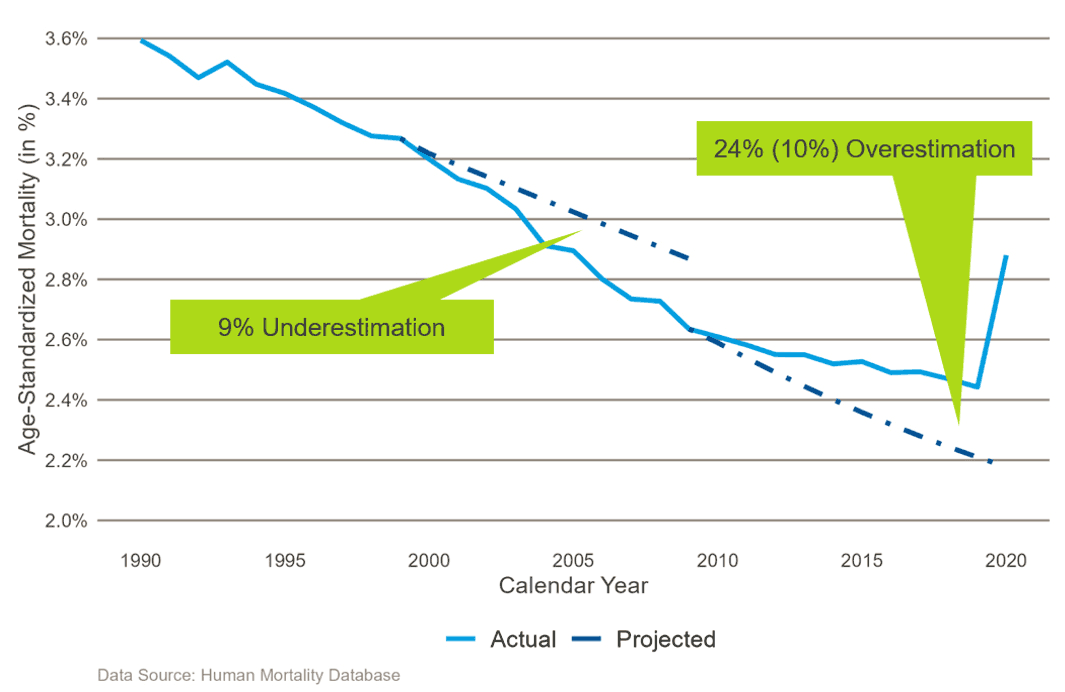

Given the complex underlying dynamics, we have to acknowledge that predicting future mortality improvements is a very difficult task—even using sophisticated models. For instance, an APC model trained on 1960–1999 US population mortality data underestimates actual improvements for the next decade by 9%, whereas a model trained on 1970–2009 data overestimates improvements by 24%—10% if the atypical pandemic year 2020 is excluded (Figure 3). It should be noted that the projections of future mortalities are based on models that are designed to reflect (some) major effects. Nevertheless, no model will be able to properly reflect all drivers of mortality. The modelled mortality must not be confused with reality.

Figure 3

Discrepancy Between Predicted and Actual Mortality Improvements for US Males.

Note: Predictions generated based on an APC model trained on US population mortality data. An overestimation of 10% results if 2020 is not considered.

Future Drivers of Mortality

Given the current increase in volatility, significant discrepancies between projected and actual mortality are likely to continue to be observed in the coming years. Another way to get a sense of future mortality trends is to identify developments and events that will affect future life expectancy. What will be potential key drivers of mortality in the coming years?

Climate change with increased periods of high temperature and a reduction of very cold times, zoonotic diseases, mRNA vaccines and socio-economic determinants are likely to be key drivers of mortality changes in the future.

One much-discussed topic is the future impact of climate change on mortality. In 2022, periods of extreme heat led to a significant number of excess deaths in the UK, Germany and other European countries. Climate change is also expected to increase the likelihood of extreme weather events such as floods, fires, and storms that can directly threaten infrastructure safety and public health. How frequently will such events occur in the future, and how well prepared are we to deal with the consequences?

Another potential consequence of climate change is the increased risk of zoonotic diseases, that are caused by viruses and bacteria that spread between animals and humans. Covid-19 is the most recent notable representative of this type of infections. Over the last months, Covid-19 has evolved from a pandemic to an endemic disease, but the long-term impacts are still largely unclear. Will there be prolonged health problems following an infection? Will we continue to see local outbreaks, perhaps with some form of seasonality as with influenza? What will be the effects of health care strains due to delayed treatments and diagnoses?

A key element in the successful containment of the Covid-19 pandemic was the effective application of mRNA vaccines. This technology came to prominence in the context of the pandemic, but has been researched for the therapeutic treatment of cancer for much longer. Advances in this field are expected to improve the treatment of cancer in the near future. In general, progress in the field of precision medicine, with more individualized treatments based on gene markers, is anticipated to reduce mortality rates in the coming years.

Socio-economic determinants have contributed significantly to a reduction of mortality in the past. Further improvements in health are also likely to be strongly influenced by efforts to change lifestyle and the environment. Disparities in mortality by socioeconomic status have increased, particularly in recent years. Closing this gap will be a crucial political task in the years ahead, especially in light of the current challenges we face.

Managing Longevity Risks

As the past years have shown how difficult it is to predict future mortality, actuaries have to ask themselves how they manage the longevity risks. There are various aspects of risk management that are relevant. For insurers’ risk management the diversification between individual risks is an important factor, allowing insurance companies to aggregate risk. Regulators demand that insurance carriers hold risk capital against the risks entered into by the insurers. Moreover, earnings volatility in the published accounts may want to be avoided, and lastly, a long-term economic view on the risks may be taken.

Unfortunately, the risk of future mortality improvements is a systematic risk affecting all longevity business in the same way. It is therefore not possible to diversify longevity improvement risks through the accumulation of more longevity business. As one can see from Figures 1 and 2, there may be some diversification across countries; however, the diversification will be limited and as the recent pandemic has shown, many developments in mortality show similar patterns across countries. One might argue that insurers offering life insurance products with longevity risks and mortality risks could hedge the improvement risk. This would be feasible in a situation where longevity and mortality risks are written for the same age groups. Hence, an annuity writer could use whole of life assurance as a means to balance some of the longevity improvement risks. As diversification is therefore of limited use in respect of longevity risks for insurers, what other options are available?

Reinsurance can be another means of managing longevity risk. Reinsurance is accepted by regulators around the world as an appropriate means of reducing risk and risk capital for insurance companies. Reinsurers often cover a wider spectrum of risks so diversification can be more achievable for reinsurers, allowing them to price longevity risks below the cost of capital for an insurer of longevity risks. Reinsurance thus reduces risk capital and earnings volatility for the insurer.

Summary

Given the current outlook, there are many reasons to expect a turbulent future. However, this was also the case in the past, and yet enormous increases in life expectancy have been achieved over the last centuries. Nevertheless, the trend has always been subject to fluctuations. In the last decade in particular, increasing volatility can be observed, which is not expected to diminish in the years to come. In view of this development, precise predictions of future mortality are associated with a high degree of uncertainty. This must be reflected in our assumptions in order to operate a sustainable and robust business.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries, the newsletter editors, or the respective authors’ employers.

Cord-Roland Rinke, FSA, is the managing director of Life & Health Analytics and Longevity at Hannover Re and can be contacted at Cord-Roland.Rinke@hannover-re.com.

Jan-Niklas Rössler is an associate data scientist for Life & Health Data Analytics at Hannover Re and can be contacted at Jan-Niklas.Roessler@hannover-re.com.