Results of the 2022 SOA Reinsurance Section Life Reinsurance Survey—Reaching an Inflection Point for Future Surveys

By Anthony Ferraro and Lloyd Spencer

Reinsurance News, October 2023

About the Survey

The SOA Reinsurance Section has completed its 2022 Life Reinsurance Survey, an annual assessment of the individual life and group life reinsurance market data of U.S. and Canadian life insurers. Survey results are based on financial information self-reported by the reinsurers of the business and include new business and portfolio production and in-force figures broken into the following categories:

- Recurring reinsurance: Conventional reinsurance covering an insurance policy with an issue date in the year in which it was reinsured. For purposes of this survey, this refers to an insurance policy issued and reinsured in 2022.

- Portfolio reinsurance: Reinsurance covering an insurance policy with an issue date in a year prior to the year in which it was reinsured (whether traditional or financial reinsurance). One example of portfolio reinsurance would be a group of policies issued during the period 2016–2019 but reinsured in 2022.

- Recurring Retrocession reinsurance: Reinsurance not directly written by the ceding company. Since the business usually comes from a reinsurer, this can be thought of as “reinsurance of reinsurance.”

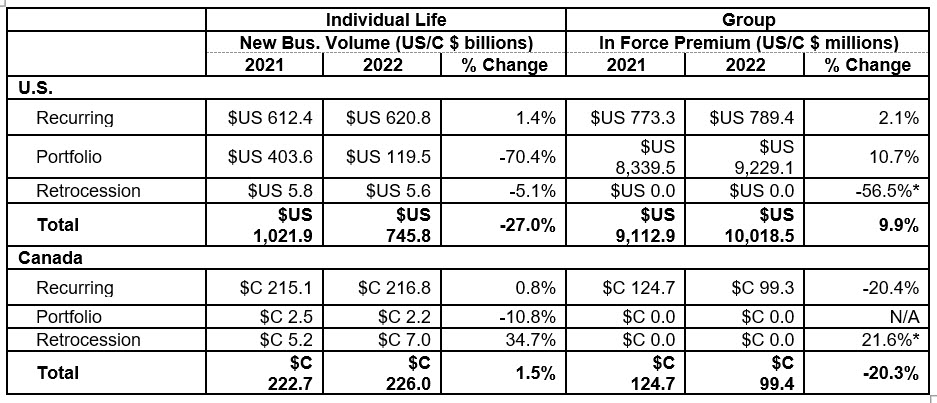

Individual life results are based on net amount at risk, while the group life results are based on premium in force. The figures are quoted in the currency of origin. All traditional life reinsurers in North America were contacted and chose to participate in this year’s survey. Table 1 summarizes the results from the 2022 SOA Reinsurance Section’s Life Reinsurance Survey.

Table 1

U.S. and Canadian Reinsurance Landscape

* NOTE: Group Retrocession amounts are too small to display

The remainder of this article discusses this year’s results in more detail, analyzes overall life reinsurance trends, and looks ahead to issues to be considered in future surveys.

United States—Individual Life

Recurring New Business

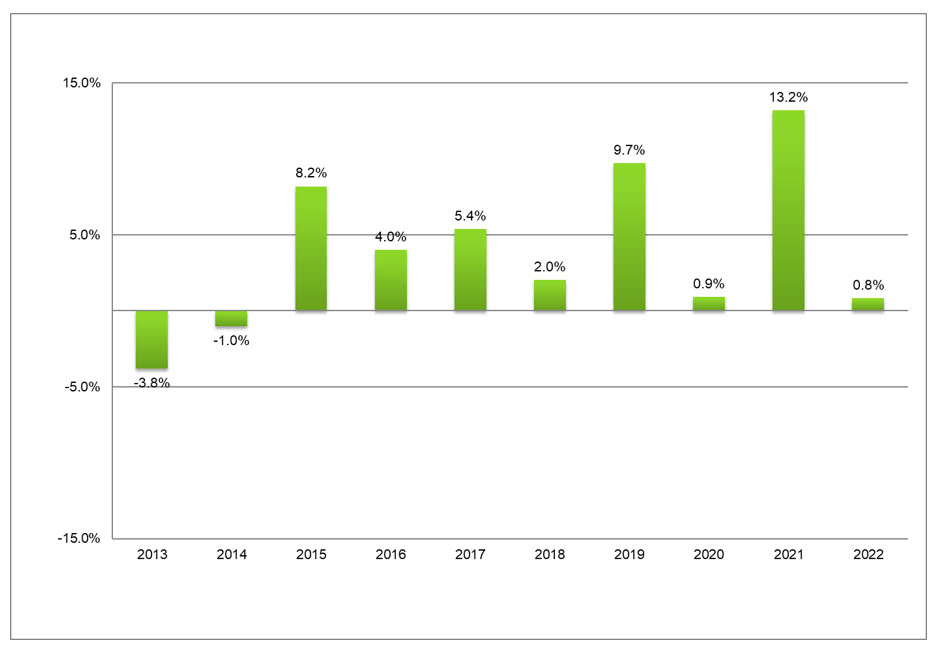

Recurring individual life new business volume in 2022 grew for the seventh consecutive year, from $US 612.4 billion in 2021 to $US 620.8 billion in 2022 (a 1.4% increase). One contributing factor to the increased volume of U.S. individual life reinsurance is the continued growth in accelerated underwriting programs, and the expansion of face amounts available under these programs. These factors elicit support from reinsurers in product and program development, as well as in risk sharing.

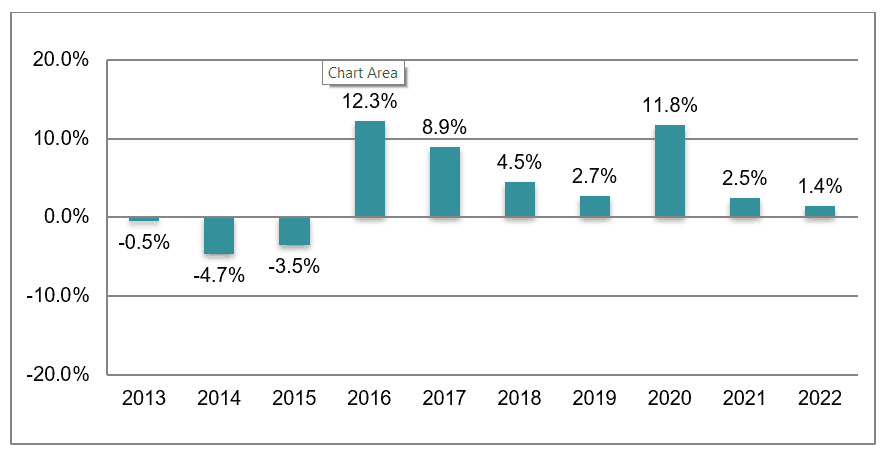

Figure 1 shows the annual percentage change in U.S. recurring new business production over the last 10 years, illustrating sustained upward trends over the past six years. Since the end of the most recent decline in the U.S. individual life reinsurance market in 2015, individual life recurring new business has grown at a compound annual growth rate of just over 6%.

Figure 1

U.S. Percentage Change in Recurring New Business 2013–2022

In 2022, 83% of recurring new business volume was yearly renewable term (YRT) and 17% was coinsurance, consistent with prior years’ survey results.

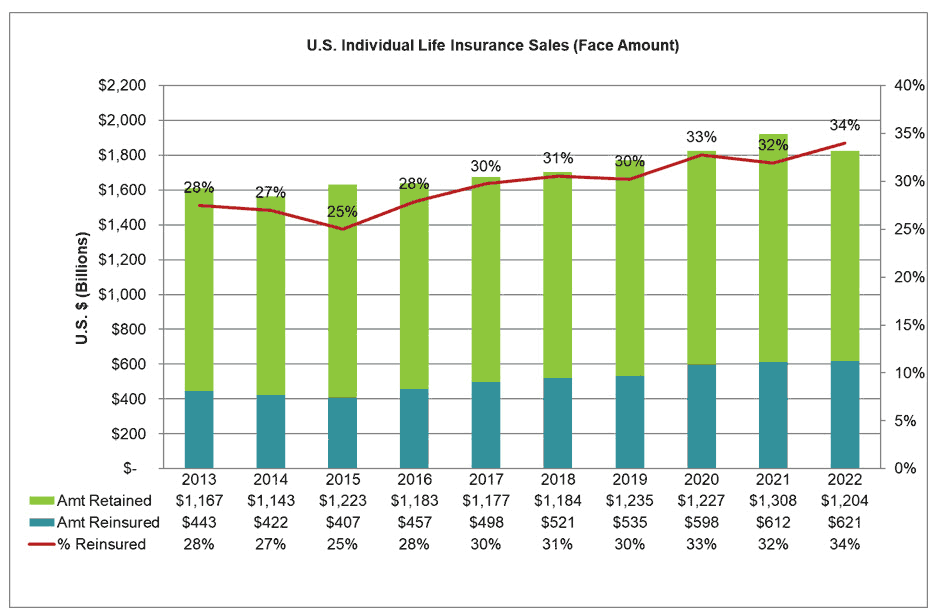

To estimate an overall cession rate for the life reinsurance industry, we compare new direct life sales to new recurring reinsurance production. According to LIMRA,[1] direct individual life insurance sales in 2022 fell by 5% (based on face amount) for the first time since 2014. Taking these results together with the surveyed life reinsurance production levels results in an estimated cession rate for the industry of 34% for 2022, the highest level since 2009. As seen in Figure 2, the estimated cession rate increased steadily from a low of 25% in 2015 to 34% in 2022.

Figure 2

U.S. Individual Life Insurance Sales ($US Face Amount)

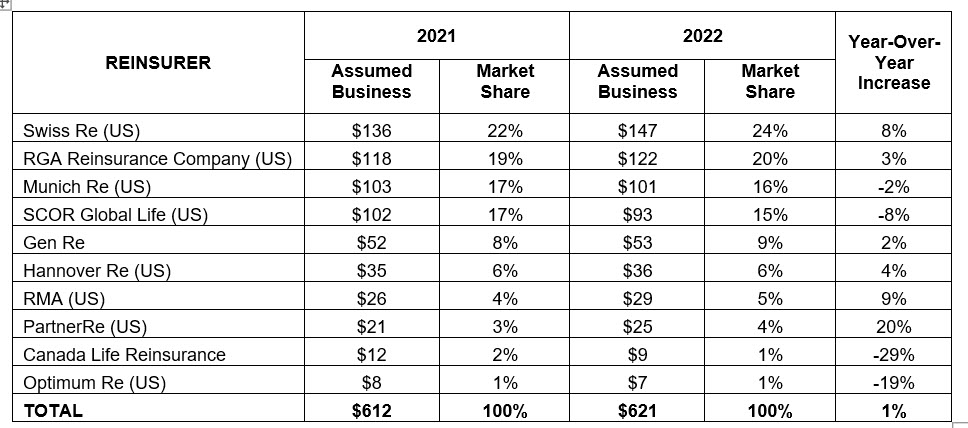

The top five U.S. individual life reinsurers by market share represent 83% of 2022 production (the same as in 2021)—see Table 2 for the information by reinsurer.

Table 2

U.S. Recurring Individual Life Volume ($US billions)

Swiss Re led all reinsurers in recurring U.S. individual life reinsurance new business volume at $US 147 billion (an 8% increase over 2021, 24% market share). The next four largest reinsurers by market share were RGA ($US 122 billion, 20% market share), Munich Re ($US 101 billion, 16% market share), SCOR ($US 93 billion, 15% market share) and Gen Re ($US 53 billion, 9% market share). Six reinsurers reported increases in recurring new business volumes versus 2021.

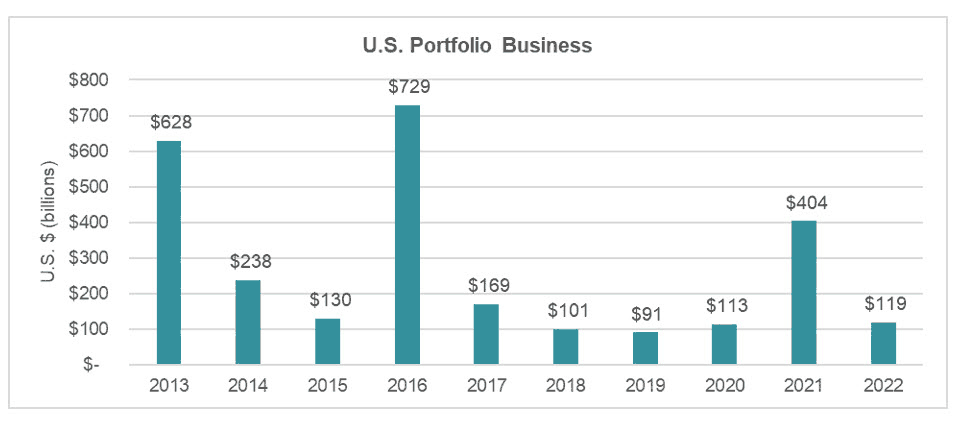

Portfolio New Business

For the purposes of this survey, portfolio reinsurance is defined to include in-force blocks of business as well as financial reinsurance transactions. This definition can produce large fluctuations from year to year in reported portfolio new business results. Portfolio new business decreased from $US404 billion in 2021 to $US119 billion in 2022. Munich Re accounted for $US98 billion (82% market share) of the 2022 portfolio new business followed by RGA at $US11 billion (9% market share) and Swiss Re at $US10 billion (9% market share).

Figure 3 illustrates the portfolio new business written over the last 10 years, which highlights the volatility of the volume of portfolio new business written in any particular calendar year.

Figure 3

U.S. Portfolio New Business Trend

New Business Retrocession

New business retrocession volumes are considerably smaller than recurring new business and portfolio new business volumes. From 2005 to 2015, retrocession production in the U.S. had been on a downswing, dropping from $US43 billion in 2005 to $US5 billion in 2015. 2022 new business retrocession volume was $US6 billion, similar to the production reported since 2016. The primary new business retrocessionaires in the U.S. include Berkshire Hathaway Group, Equitable, and Pacific Life Re.

There was a significant transaction (in terms of retrocession volume) that occurred during 2022 that was atypical of recent retrocession market activity, both in the nature of the transaction and the volume of business written. The SOA Reinsurance Section Council discussed this transaction and decided to exclude it from the 2022 survey primarily due to the portfolio retrocession nature of the transaction (as opposed to the new business retrocession typically reported in this category of the survey). The business was written prior to 2022 by a U.S. direct life insurer and ceded outside the North American reinsurance market. In 2022, the business was retroceded to a U.S. reinsurer. Future surveys will include any such transactions in a separate category called “Portfolio Retrocession.”

Canada—Individual Life

Recurring New Business

Recurring individual life reinsurance new business in Canada increased for the eighth consecutive year in 2022, growing from $C215 billion in 2021 to $C217 billion in 2022 (up 1%). Figure 4 shows the annual percentage change in recurring reinsurance new business over the last 10 years. Since 2015, recurring Canadian new business has grown at a 6% compound annual growth rate.

Figure 4

Percentage Change in Recurring Canadian Individual Life Reinsurance New Business 2013–2022

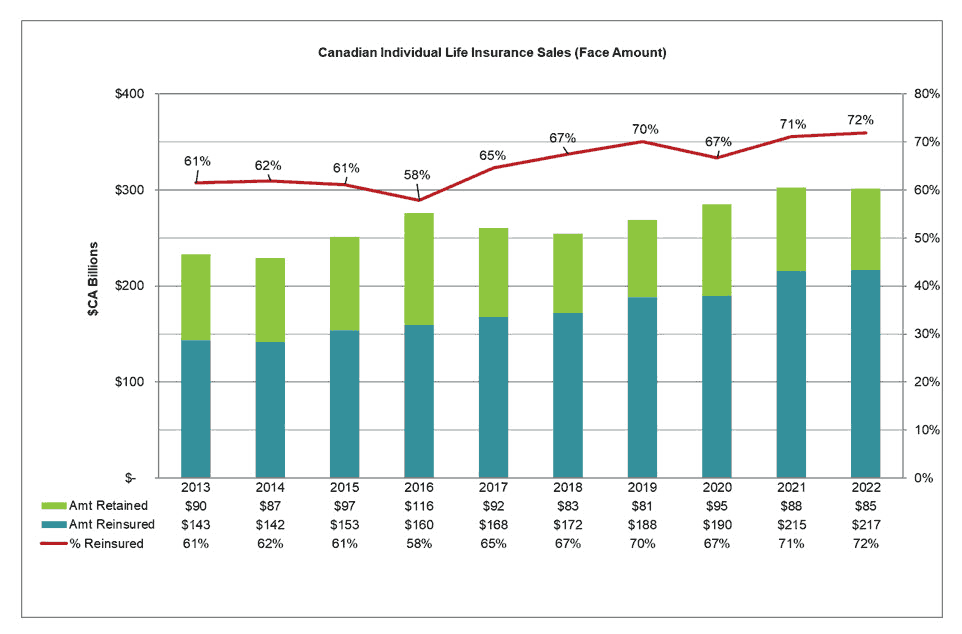

According to LIMRA[2], Canadian direct individual life sales (on a face amount basis) decreased less than 1% in 2022 when compared to revised 2021 data, the first decrease reported since 2018. The estimated cession rate for 2022, which is based on a comparison of direct life sales to recurring reinsurance volumes, increased slightly from 71% in 2021 (based on revised data) to 72%. The 2022 cession rate is the highest reported cession rate since 2009. Canadian cession rates continue to be much higher than those in the U.S.

Figure 5

Canadian Individual Life Insurance Sales (Face Amount)

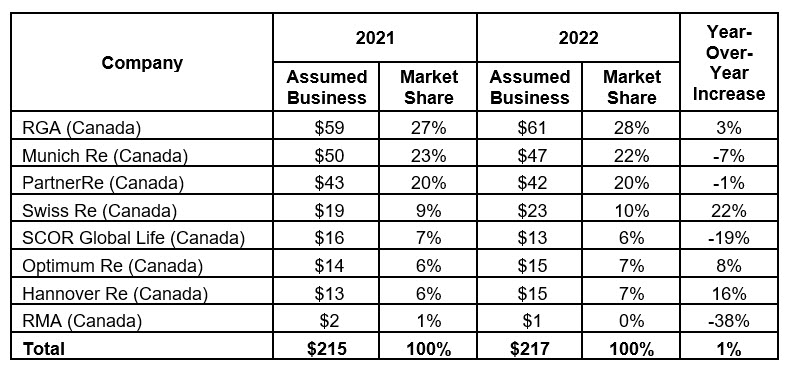

The top three individual life reinsurers in the Canadian market during 2022 (based on market share) were RGA, Munich Re, and PartnerRe. Together, these three reinsurers hold a 69% market share. RGA topped recurring new business writers reporting $C61 billion of written volume in 2022 (up 3% over 2021). Munich Re followed with $C47 billion (7% decrease from 2021), followed by PartnerRe with $C42 billion (1% decrease from 2021). Of the eight reinsurers reporting in the 2022 survey, four reported increases in recurring new business volumes from 2021 to 2022. Table 3 summarizes assumed volumes and market share by reinsurer for 2021 and 2022.

Table 3

Canada Recurring Individual Life Volume ($C Billions)

Portfolio New Business

Munich Re reported portfolio new business in 2022 totaling $C2.2 billion. RGA also reported a nominal amount of portfolio new business as well that rounded to $C0.0 billion.

New Business Retrocession

New business retrocession in Canada is considerably smaller than recurring new business and portfolio business. Canadian retrocessionaires active in 2022 included Pacific Life Re and Berkshire Hathaway, with Pacific Life Re writing $C4.5 billion and Berkshire Hathaway writing $C2.4 billion. Overall, the new business retrocession market in Canada grew this year from $C5.2 billion in 2021 to $C7.0 billion in 2022.

United States—Group Life

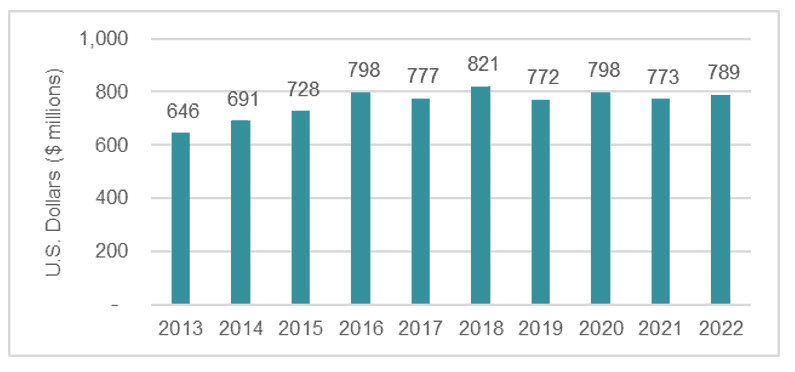

U.S. group life reinsurers reported $US10.0 billion of in-force premium at the end of 2022, up 10% from the $US9.1 billion reported at the end of 2021. Recurring new business accounted for $US0.8 billion of the total, up 2% when compared to 2021, while portfolio business and a very small amount of retrocession accounted for the remaining $US9.2 billion balance.

According to data presented in Figure 6, recurring new business in force grew 22% from year-end 2013 to year-end 2022, which represents a compound annual growth rate of 2%.

Figure 6

U.S. In-Force Recurring New Business Group Premiums ($US Millions)

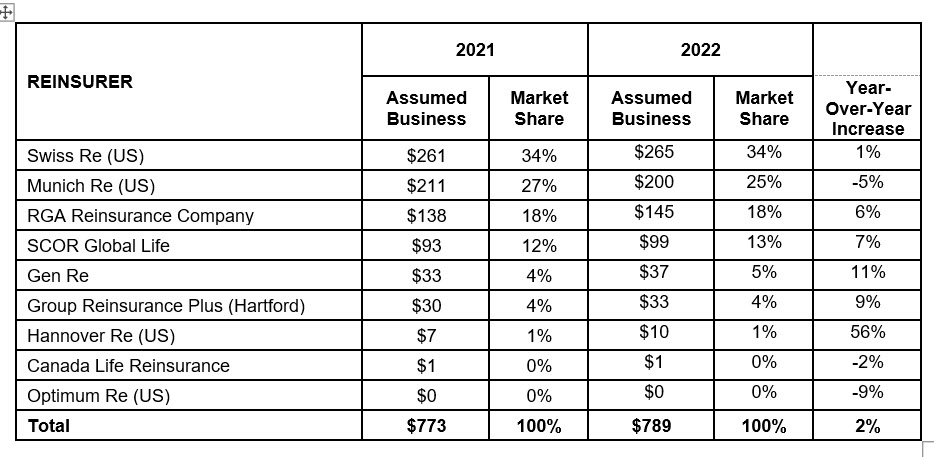

As illustrated in Table 4, the top four reinsurers in this market are Swiss Re, Munich Re, RGA, and SCOR. Collectively, these reinsurers account for a 90% market share.

Table 4

U.S. Traditional In-Force Group Premiums ($US Millions)

In-force group portfolio premium totaled $US9.2 billion in 2022, up 11% from the $US8.3 billion for 2021. Canada Life Reinsurance reported $US8.7 billion in portfolio premium in 2022, up from the $US7.8 billion reported in 2021. Munich Re reported $US0.5 billion in 2022, unchanged from its reported 2021 value.

Canada—Group Life

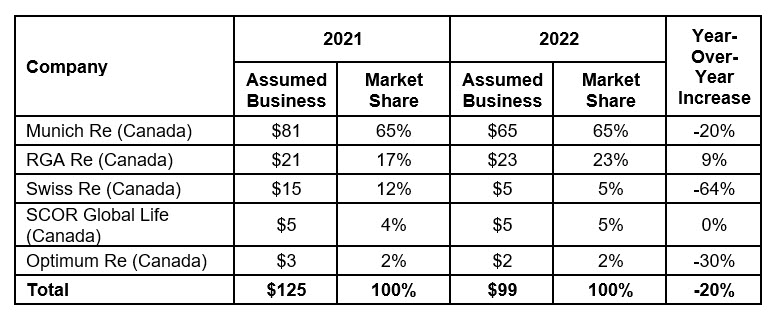

Group life reinsurers reported $99 million of in-force premium at year-end 2022, down 20% when compared to year-end 2021 levels. The group life market in Canada is dominated by Munich Re and RGA, who together account for an 88% market share (see Table 5). Of the five reinsurers reporting material volume, three reported decreases in traditional in-force premium at year-end 2022 versus year-end 2021.

Table 5

Canada Traditional In-Force Group Premiums ($C Millions)

Have We Reached an Inflection Point for Future Surveys?

Future life reinsurance financial results in 2023 and beyond will be influenced by a range of factors, including the continuing evolution of U.S. and Canadian mortality experience, developing economic factors such as inflation and interest rates, expansion of accelerated underwriting programs, changing technology, regulatory, legal and accounting landscapes, and continued mergers and acquisitions activity in the individual life insurance and annuity space. Life reinsurers are positioned to provide effective support for direct life insurance companies in addressing the challenges posed by these factors. Reinsurers’ expertise goes beyond traditional mortality and risk selection and includes financial reinsurance as well as value-added expertise in areas such as product development, underwriting operations, predictive analytics and risk selection, post-issue monitoring, and risk management. This expertise and support can be invaluable to direct writers as many look to expand their offerings, improve their outreach to consumers, and enhance controls. Reinsurance also remains a valuable tool for efficient capital and volatility management. Financial reinsurance structures and reinsurance of in-force blocks, either for non-core businesses or as a means to manage profitability, also continue to be attractive levers for direct writers.

In recent years, the traditional life reinsurance market has evolved as new entrants assume portfolio annuity and, more recently, portfolio individual life insurance blocks of business. These entrants use reinsurance as a tool to bring assets to their investment portfolios while providing capital and surplus relief to the direct life insurance company from which the business is reinsured. Consideration by the SOA Reinsurance Section Council of the impact these companies have on the U.S. and Canadian reinsurance markets may signal that changes to future SOA Reinsurance Surveys could be forthcoming.

Thank you to all the reinsurers that participated in this year’s survey. Complete results are available on the Munich Re website.

Note that Munich Re prepared this survey on behalf of the Society of Actuaries Reinsurance Section as a service to section members. The contributing companies provide the data in response to the survey. The data is not audited, and Munich Re, the Society of Actuaries and the Reinsurance Section take no responsibility for the accuracy of the figures.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries, the newsletter editors, or the respective authors’ employers.

Anthony Ferraro, FSA, MAAA, is senior vice president, Individual Life Reinsurance at Munich Re. He can be reached at aferraro@munichre.com.

Lloyd Spencer, FSA, CERA, is senior market intelligence lead, Individual Life Reinsurance at Munich Re. He can be reached at lspencer@munichre.com.