7702A Reduction in Benefits Testing: A Simplified Approach

Part 1: Reductions in Death Benefits

By Larry Hersh

Taxing Times, March 2022

Overview

In 1988, Section 7702A was added to the Internal Revenue Code of 1986.[1] A policy that qualifies as life insurance under Section 7702 may be classified as a Modified Endowment Contract (MEC) if the premium payments received under the contract fail the Seven-Pay test. A MEC continues to receive favorable tax treatment for the death benefit, but distributions are taxed on an income-first basis.

Section 7702A(c) provides detailed computational rules, including rules that apply when there is a Reduction In Benefits[2] (RIB) under the contract within the first seven years of contract issue or following a material change.[3] For survivorship contracts, the RIB period is extended and applies over the lifetime of the contract.[4]

If a policy has an RIB that is subject to RIB testing under Section 7702A(c)(2), the policy is retested for MEC status retroactively to the start of the Seven-Pay testing period using a Seven-Pay Premium that is reflective of the reduced benefits. If the policy’s premiums would have failed the Seven-Pay test based on the reduced Seven-Pay limit, the policy is classified as a MEC.

Insurers are required to administer to this provision, and have dutifully done so by creating systems and procedures necessary to both detect when a RIB has occurred and to determine if the policy would be classified as a MEC.

In applying the Seven-Pay test to a policy undergoing an RIB, a typical practice is to calculate the reduced Seven-Pay Premium based on the reduced benefits and then reapply the Seven-Pay test. The test is performed by applying the policy’s actual premium and withdrawal history against the Seven-Pay limit based on the reduced Seven-Pay Premium. This would allow the insurer to identify the policy as a MEC and if so to determine if the policy can be brought back into compliance.

Such retroactive testing can be administratively difficult, requiring that the financial history for the policy is available at all times necessary to support RIB testing. For a Universal Life policy, where the premiums are flexible, accessing the financial history data to perform this test can be challenging. Another complication, specific to survivorship policies is that the RIB that triggers RIB testing may be many years after the Seven-Pay testing period has ended. Thus, the financial transaction data necessary for reapplying the Seven-Pay test must be maintained over a potentially very long period of time.

This article proposes an alternative method for applying RIB testing to a contract that is mathematically equivalent to the more traditional method described above. However, the alternative method does not require access to detailed financial transaction history, providing a more streamlined approach for RIB testing. Some potential advantages of this method include:

- This method requires only cumulative premiums paid data for RIB testing, without the need for the exact timing and amount of each financial transaction.

- It allows for the determination of a minimum death benefit amount—the Reduction in Benefits Face (RIBFace)—which would be the reduced amount of death benefit that could be supported under an RIB that would not cause the policy to be a MEC.

- The method provides an incremental “cost” to a policyholder by relating how a premium payment may limit the amount of any future RIB for avoiding MEC status.

The alternative method breaks down the RIB testing process into three parts, each of which “drills down” further when necessary to do so:

- MEC Determination: An alternative test to determine MEC status can be performed that is based on the amount that benefits are reduced, rather than by comparing the premiums paid to a Seven-Pay limit.

- MEC Re-compliance: If the RIB would cause the policy to become a MEC, then a second determination is performed to determine whether the policy can be brought back into compliance under the 60-day rule of Section 7702A(e)(1)(B).[5] If so, then access to the detailed premium history would be required to determine the amount of excess premium that must be returned with interest to the policy owner.

- Non-MEC Testing Limits: If the RIB is determined to not result in the policy becoming a MEC, then the insurer re-computes the reduced Seven-Pay testing limit according to their current practices and monitors the policy for compliance with the Seven-Pay test on a going-forward basis.

In effect, the alternative method described in this article is possibly “another tool in the toolbox” that an actuary can consider for their Seven-Pay practices. Such a consideration must take into account the type of business being sold, the nature of the administrative systems, and the policy data that is available.

This is the first part of a two-part series. In this article, the alternative method will be outlined in detail as it would apply to a reduction in death benefit. Part 2 will consider the changes necessary to accommodate a reduction in Qualified Additional Benefit (QAB) riders.[6]

Setup: Basic Formulas and Assumptions Used

The alternative method requires certain values be computed and stored in the system and be available at any time that a reduction occurs. These values are necessary for assessing the effect of an RIB and applying the RIB test, under both the traditional and alternative approaches:

- The ability to detect an RIB event.

- The present values of the benefits used as of the Seven-Pay test start date.

- The presence of a 1035 premium or other amount spread in the Seven-Pay Premium upon a material change. The term Tax Cash Value (TCV) will be used for this purpose.

- The sum of premiums less nontaxable withdrawals used in conducting the Seven-Pay test.

All of these would be necessary to perform the RIB calculations under either approach. The job of the tax actuary is to adapt the formulas and methods described in this article to fit within the company’s processing of Seven-Pay testing. The formulas provided here are therefore general in their construction.

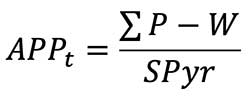

Equation 1: Average Premium Paid

Step 1 is to determine the Average Premium Paid (APP) at the time of each premium payment (or withdrawal) during the Seven-Pay testing period. APP uses the “amount paid” as defined in section 7702A(e)(1)(A),[7] which is generally equal to the sum of the gross premiums paid (P) less non-taxable withdrawals (W). However, in defining APP for use in the RIB test, the amount paid at any point in time is divided by the Seven-Pay testing year (SPyr) thus creating an annualized average payment over the testing period. So, at each point (t) where a premium is paid, or a withdrawal taken, the APP can be determined as follows:

The APP can either be stored on the system, or calculated directly at any time that a financial transaction is processed that results in a change the amount paid, just as would be done for the Seven-Pay limit test. The use of AAP replaces the need to use the detailed premium history in the determination of MEC status.

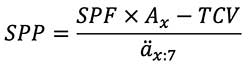

Equation 2: Standard Seven-Pay Premium Formula

This formula is provided as a reference to help define the terms that will be used throughout the article.

Where:

- SPP = Seven-Pay Premium

- SPF = Assumed Seven-Pay Face Amount

- TCV = Tax Cash Value (i.e., the “roll over” cash value for policies issued pursuant to a Section 1035 exchange of the cash value used in the calculation of the SPP for a materially changed contract)

- Ax= net single premium for $1 of death benefit, calculated as part of the Seven-Pay Premium determination

- äx:7 = annuity factor assuming $1 payable at the beginning of each year of the Seven-Pay testing period

These are all standard formulas that are used in the calculation of a Seven-Pay Premium. The equation solves for the maximum premium allowed for a given face amount that if paid annually, would allow the contract to remain a non-MEC.

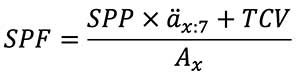

The next formula effectively reverses the calculation from the determination of a stated premium (i.e., the SPP) to the determination of death benefit (i.e., minimum SPF). It is this formulation that is the basis of the alternative RIB Method, and allows this to method to produce identical results.

Equation 3: Solving for the Seven-Pay Death Benefit

For a given SPP, the solution for a minimum SPF that would be a non-MEC is as follows:

RIB Method for Death Benefit

Step 1: Determination of MEC Status

When using a more traditional testing approach, the Seven-Pay limit based on the reduced SPP is compared directly to the premium history over time. The advantage of this method is that it provides the three critical pieces of information necessary to complete RIB testing:

- It determines if the policy would become a MEC.

- If the policy is a MEC, then determines the timing and amount of the excess premium that lead to failure and whether the policy could be put back into compliance.

- If it is not a MEC, it resets the Seven-Pay testing limits accordingly.

What the alternative method proposed herein does is answer each of these questions separately.

The first component of the alternative method involves determining if the policy would fail the Seven-Pay test and attain a MEC status. To do so does not provide the exactness of the traditional test. In effect, it does not matter if the policy fails the test by $1 or by a much larger amount. The first part of the alternative method simply determines that a failure would occur.

To make the MEC determination (i.e., did the RIB result in the contract becoming a MEC), and to reduce the amount of premium data that is necessary for making this determination, the MEC determination is based on identifying the lowest level of benefits that could be supported based on the premiums historically paid, rather than evaluating the historical premiums when compared to the reduced Seven-Pay limit.

Equation 4 provides a formula that will be used to solve for the death benefit that can be supported for the historical premiums paid. Such a death benefit would be the minimum allowed without the policy becoming a MEC based on the sum of premiums paid at that time. By construction, Equation 4 is mathematically identical to the solution for a SPP.

Said simply, if the owner paid a premium equal to the Seven-Pay Premium, then their face amount cannot reduce below Seven-Pay Face without becoming a MEC.

However, these are limitations based on the policy as it was issued. Instead of using the formula to identify that maximum face amount that can be supported by the payment of a SPP such that the contract will not become a MEC, the formula substitutes the APP and then solves for the minimum face amount (MinFace) required for the Seven-Pay test to be passed at any given point in time (t).

Equation 4: Minimum Face Amount for a Given APP

The MinFace used here provides (at any point in time t) a measurement of what Seven-Pay benefits can be supported by the premiums paid at that time. For example, if the policy owner paid an initial premium equal to the Seven-Pay Premium (i.e., AAP = SPP), then the MinFace would exactly equal the Seven-Pay Face. If the premium was greater than this amount (i.e., APP > SPP), then the MinFace would exceed the SPF and the policy would become a MEC, analogous to the premiums exceeding the Seven-Pay limit.

This is where the alternative method “turns it on its head” in identifying the minimum death benefit for preventing the policy from becoming a MEC rather than the determining whether a policy would become a MEC based on actual premiums paid and the reduced level of benefits. For RIB purposes, the RIB test under the alternative method is not concerned with what the maximum face amount is, but rather what the minimum face amount would be for avoiding MEC status. It is as if the owner asked the question “How much can I reduce my benefits to?”

To make the MEC determination, the answer to that question needs to be asked on a worst-case basis. To do so, a RIBFace is defined as follows: At any time that a premium is paid, or a withdrawal is taken (i.e., the amount paid has changed), calculate the MinFace using Equation 4 to avoid the contract from becoming a MEC and set the RIBFace amount according to Equation 5.

Equation 5: Reduction in Benefit Face Amount (RIBFace)

![]()

Why this works:

- The MinFace calculated in Equation 4 represents the minimal death benefit that would avoid MEC status at the time a premium is paid.

- The RIBFace amount in Equation 5 is the highest value during the Seven-Pay testing period that the death benefit can be reduced to without resulting in the contract becoming a MEC over the entire testing period. This value corresponds to the point in time during the Seven-Pay testing period where the premiums are at their zenith relative to the Seven-Pay testing limit.

- The difference between the SPF and the RIBFace amount represents the amount of additional benefit that would be allowed under the Seven-Pay test before the policy would become a MEC. Conversely, this is the same as determining the amount of additional premium that could have been paid up to the Seven-Pay limit.

The RIBFace measures the amount of the death benefit below which the policy would fail the Seven-Pay test if the benefits are reduced below this amount at any time during the test period. To the extent the death benefit reduces below the RIBFace, the alternative method does not provide the amount by which the amount paid exceeds the Seven-Pay limit, or the specific date when the amount paid exceeded the Seven-Pay limit for the first time.

At the time of an RIB Event, the determination of MEC Status only requires access to two values: APP and the RIBFace amount. What is not required to determine the MEC status is the detailed history of premium and withdrawal transactions. Those transactions become important in the following two steps.

Step 2: Ability to Re-comply a MEC policy upon a Reduction in Benefits

Section 7702A(e)(1)(B) provides that a policy can be restored to a non-MEC status if “any portion of any premium paid during any contract year is returned by the insurance company (with interest) within 60 days after the end of such contract year.”

Companies have monitoring systems and procedures in place to determine if a policy is a MEC and if the MEC date falls within this 60-day period.

As with the determination of MEC status, it is not necessary to determine the exact amount and timing of the premium that violates upon a reduction retest. The first order of business is to simply determine if a policy can be re-complied under the statute.

A simple example is a survivorship policy, where the RIB rule extends beyond the Seven-Pay testing period.[8] If such a policy is in year nine and the policyholder elects to reduce benefits below the RIBFace, then the determination of when the policy becomes a MEC and by how much is moot; the policy is a MEC.

The first step in determining MEC Status does not, by itself, determine the date that the policy would fail, and thus does not answer the question about an ability to re-comply. However, this can be tracked under the alternative method by tracking the RIBFace over time. An example of how this may be done is as follows:

- Store the RIBFace on an annual basis for each test year.

- The payment that caused the MEC to arise occurs in the earliest year where the reduced death benefit is less than the RIBFace.

- If that is not during a year with the Seven-Pay testing period where re-compliance is possible, then the policy is a MEC.

- In the event that the policy is in a period where it can be re-complied, then calculate the Seven-Pay Premium using the reduced death benefit and proceed to retest the historical premiums to identify the date when amounts paid exceeded the Seven-Pay limit based on the reduced Seven-Pay Premium.

Note that it may still not be possible to restore the policy to a non-MEC status. However, if the benefits are reduced so that there would be multiple failures over time, a prior period failure may still prevent re-compliance and the policy would be a MEC.

The idea of breaking up the process into two steps is to further reduce the amount of policies that need to go through the exercise of being fully retested for compliance with the Seven-Pay test by removing those where non-MEC status cannot be restored. However, it is always a good practice to review, validate and communicate MEC status with any policy owner.

Step 3: Reductions where the policy is not a MEC

If the RIB is such that the reduced death benefit exceeds the RIBFace amount, then the RIB would not cause the policy to become a MEC.

All that is required is to use existing procedures to reset the SPP and re-determine the Seven-Pay limit along with and any other values that the carrier calculates based on the actual benefits used. This can be done using existing system techniques. No retesting would be required.

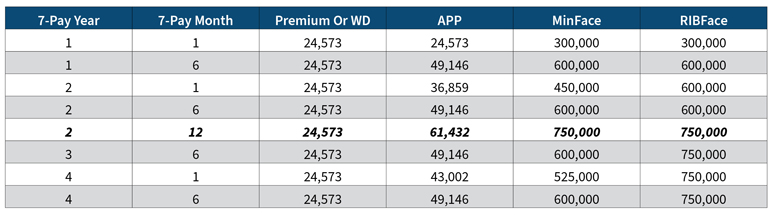

Example 1: Reduction in Death Benefits

Mr. Owner is a 50-year-old male who takes out a policy with a $1,000,000 death benefit at issue. His intent is to pay 60 percent of the SPP each year, to be paid in semi-annual installments. However, in year two, he pays his semi-annual premium just prior to the anniversary. Paying this premium amount would not cause the contract to fail the Seven-Pay test.

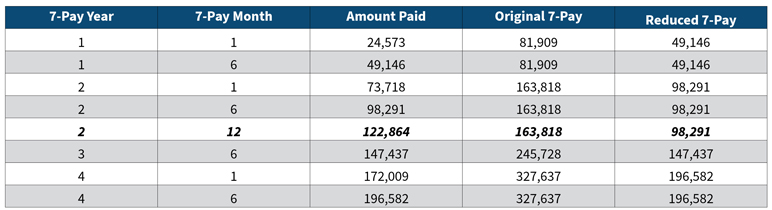

Between policy years one and four, the policy transactions are tracked as shown in Table 1.

- In the first policy year, the payment of a 60 percent SPP corresponds to a 60 percent RIBFace amount (i.e., 60 percent of the initial death benefit, or $600,000).

- At the start of year two, the minimum face amount would drop as AAP reduces from $49,146 to $36,859, but the RIBFace does not.

- The early payment at the end of year two, however, has the effect of increasing the RIBFace amount to $750,000 as AAP increases to its highest level.

Table 1

Calculation of the RIBFace under the Alternative Method

To continue, assume that Mr. Owner wants to reduce his benefit to $600,000 at the start of policy year five, on the assumption that he paid 60 percent of the SPP annually (and therefore he would assume that the policy would not be a MEC as a result of this RIB).

This would not be the case, as illustrated below in Table 2. Table 2 represents the effects of both Steps 1 and Step 2, determining the MEC status and the ability to re-comply under the 60-day rule. The system processes the transaction as follows:

Under the proposed method:

Step 1. The reduced benefit of $600,000 is less than the $750,000 (the highest RIBFace over any point in time during the Seven-Pay testing period). The policy is identified as a MEC.

Step 2. The year in which the RIBFace was set to $750,000 was in year two. As any point in time in year two is not within a 60-day period (in year five), the policy cannot be brought back into compliance.

Note: If the contract provided language that would not allow the transaction to occur (e.g., the contract language would prohibit a reduction in benefit without prior written approval from the policyholder, and the policyholder had not provided written approval), a message to the owner offering the $750,000 minimum would be possible.

Table 2

RIB Test under the Alternative Method

Table 3 shows the traditional method for RIB testing where historical premiums are tested for compliance with the Seven-Pay limit based on the reduced SPP. In this case, once the RIB test reduces the SPP and retests each premium for compliance with the Seven-Pay test it would similarly identify the premium in year two, month 12 as the cause of the violation.

Table 3

RIB Test under the Traditional Method

Note that although the traditional method provides the same testing result, it does not provide the amount of the reduced benefit that would be acceptable to avoid a MEC classification (i.e., RIBFace).

Further Observations

The demonstrations and formulas above show that the alternative method suggested here can produce identical results to a more traditional premiums-based approach. The question that an actuary needs to consider in evaluating this method for a company’s systems should also consider some other potential benefits.

The most important benefit of this method is the fact that it does not rely on storing or recreating the premium history on a policy. This history is only needed in the event that the policy can be brought back into compliance under the 60-day rule.

This method may also be useful in policyholder illustrations, depending on how the illustration system operates. That said, under the traditional method, the requirement of the premium history being provided from an administrative system to a separate illustration system can pose administrative difficulty. However, since the alternative method only requires the cumulative AAP amount and the current RIBFace, this reduces the amount and complexity of the data being downloaded from the administrative system to the illustration system.

There are also potential benefits in policyholder servicing. The RIBFace represents the answer to the question “How much can I drop my benefits to?” Having this amount available on the system allows an insurer’s servicing unit to provide this answer before a benefit reduction is requested or even illustrated.

On the other side, the alternative method shows an implied “cost” to the owner that may be useful. Even though premiums may be acceptable under a Seven-Pay limit, the payment of premiums has a direct limitation on the ability to reduce benefits. It acts as an opportunity cost to the owner of the policy.

For example, consider a premium that is paid a few days before a policy anniversary but where the premium does not trigger an immediate MEC status, such as in Example 1. There is an implicit cost to the owner in terms of the limitation placed on what benefit reductions are possible. For a survivorship policy, where the lifetime reduction-in-benefits rule applies, this can be very limiting many years after the premium is paid. Could the change in the RIBFace be worked into an administrative practice to communicate this to the owner? There would be many considerations of such a practice, depending on the type of policy being sold, the policy language and other administrative constraints.

Answers to questions like these are complex. The method of RIB testing here does not provide a perfect solution to all considerations. System limitations, contractual language, the types of business being funded and administrative practices all require careful thought by the actuary. However, a method such as the one proposed here may prove useful as it provides another tool that the tax actuary may consider using in designing administrative practices and systems for the Seven-Pay test.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries, the editors, or the respective authors’ employers.

Larry Hersh, FSA, is an actuary who has focused on product tax compliance and product design. He can be reached at lmh.j.mail@gmail.com.